Insights

Capital Allocation in Private Markets: How It Works and Why It Stays Inefficient

Capital allocation in private markets: why it stays inefficient and how shared infrastructure speeds allocation and widens investor participation

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Capital allocation in private markets is not just an investment decision - it is an infrastructure problem. Manual onboarding, compliance, and record-keeping keep minimum tickets high and investor access narrow, while shared digital infrastructure can reduce operational friction, speed up funding, and make smaller, compliant allocations economically viable.

Capital Allocation in Private Markets: How It Works and Why It Stays Inefficient

For most wealth and asset managers, the hard part of a private markets co-investment is not choosing it, instead it’s the weeks of manual subscription paperwork, investor onboarding, and reconciliation that follow. Capital allocation is the decision about where investable capital goes and the operational process of moving it there. In private markets that second half is slow, manual, and open to only a narrow set of investors. This guide explains what capital allocation means, why the private-market version carries so much friction, and how shared digital infrastructure speeds it up without changing the underlying regulation. It is written first for multi-family offices and wealth managers, and for the investor networks and vehicle operators who carry the same operational load.

What capital allocation means

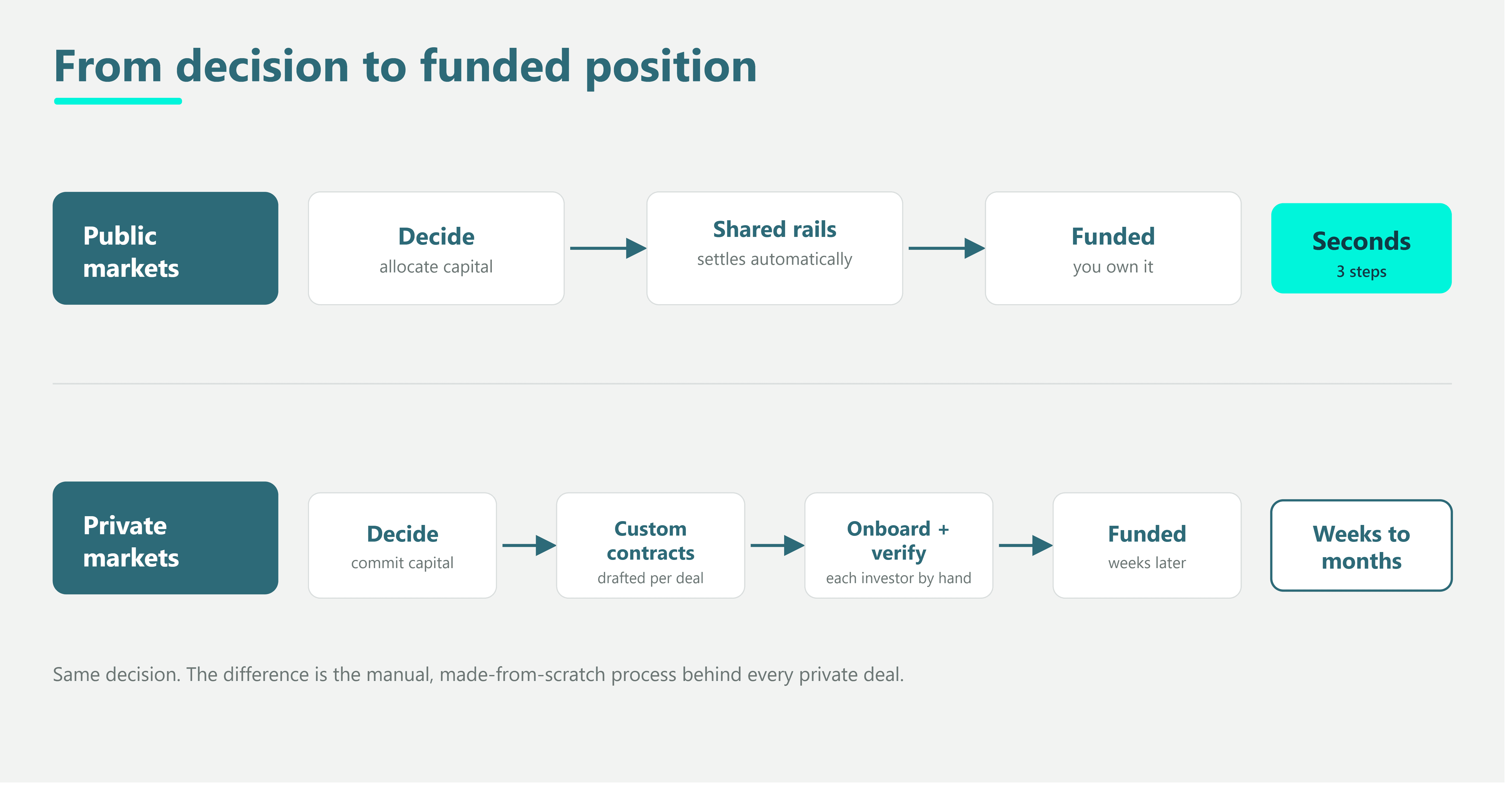

At its simplest, capital allocation is the decision about how a pool of money is distributed across opportunities, weighed against risk, return, liquidity, and mandate. In public markets, that decision is executed in seconds. In private markets, the same decision can take months to act on, because the allocation is only the first step. After the "yes" comes subscription, documentation, KYC, funding, and record-keeping, each handled by a different party.

Allocating private capital versus public markets

Public and private markets don't differ in the idea of investing. They differ in the infrastructure.

When you buy something in public markets (like a stock), it runs on shared rails everyone already uses. The paperwork, the settlement, the record of who owns what all happens automatically through standard systems. You decide, you buy, done.

Private markets have no shared rails. Every deal gets built by hand, from zero, each time: custom contracts, manually signing up and verifying each investor, and spreadsheets to track who put in how much money. The deal itself might be great, but all the manual setup between "yes, let's do this" and "the money is actually in and working" is where the time and money get eaten up.

Why is capital allocation inefficient in private markets?

Three structural frictions explain most of the drag:

Intermediation - Every additional party between the allocator and the asset adds cost, handoffs, and reconciliation.

Minimum ticket size - Onboarding one investor costs roughly the same whether they commit ten thousand or ten million, so operators rationally set high minimums, which narrows participation.

Illiquidity - Once capital is allocated, there is rarely a clean way to exit before the end of the term, so allocators price in a lock-up premium and commit less than they otherwise would.

The effect on private capital formation

These frictions don't just annoy operators; they shape outcomes:

High minimums keep smaller investors out, concentrating private capital formation among a few large players.

Long lock-ups discourage first-time allocators.

The result is a market that funds fewer projects than demand would support, simply because the operational cost of a broader investor base is too high to carry by hand.

A capital allocation strategy built on shared infrastructure

The fix isn't a new kind of investment. It's a shared system that handles the same setup steps that get rebuilt from scratch for every deal today. When sign-ups, compliance checks, and the list of who owns what all run on one common system, adding another investor costs almost nothing extra, and that one change makes everything else possible.

Smaller minimums, more investors

When a position can be split into smaller, legally compliant pieces, the minimum investment stops being a problem. An allocator can take in both big and small commitments without piling on extra admin work, because signing up and tracking every investor works the same way regardless of size. This isn't really about opening deals to the general public. It's about letting existing clients join with smaller amounts without hiring more operations staff. A small piece costs no more to manage than a large one.

Automatic compliance, faster deals

The bigger saving is in compliance. When the identity checks (KYC and AML), eligibility rules, and transfer restrictions are built into the system instead of done by hand, the gap between deciding to invest and actually being funded can shrink from weeks to a few days. The legal requirements stay the same; only the way they're carried out changes. In practice, that means a digital sign-up process, automatic investor checks, a live ownership record, and audit-ready files, which is exactly what our digital securities infrastructure provides. A 20-investor co-investment deal that used to take six weeks of back-office work to close can now close in a fraction of that time.

Broader investor participation and access to capital markets

Lowering the operational cost of an investor has a second effect: it widens who can participate. Broader investor participation is not a fairness slogan here; it is a direct consequence of cheaper onboarding. When the cost of admitting an investor approaches zero, there is no operational reason to exclude smaller commitments, and access to capital markets extends to participants who were previously priced out by minimums rather than by risk appetite.

Investor participation beyond institutional allocators

For an asset or wealth manager, this means a co-investment can be offered to a broader client base without a proportional increase in back-office work. For an investor club or network, it means a growing membership can be activated as a genuine allocation engine rather than a mailing list. The infrastructure carries the load that used to fall on people. For readers new to the terminology, our glossary defines the core terms used across private-market structuring.

Traditional versus digital capital allocation models

Dimension | Manual allocation | Shared-infrastructure allocation |

|---|---|---|

Time from decision to funded | Weeks to months | Days |

Cost per additional investor | Roughly constant, high | Approaches zero |

Practical minimum ticket | High | Low |

Investor base | Narrow | Broad |

Audit trail | Reconstructed manually | Recorded by default |

Conclusion: capital allocation is an infrastructure question

The quality of a capital allocation decision is a matter of judgment, and no infrastructure replaces that. But the speed, cost, and reach of executing that decision are matters of infrastructure, and those are solvable today. Operators who treat allocation as an infrastructure problem rather than a per-deal project widen their investor base and shorten their funding cycles without taking on new regulatory risk.

If that is the direction you are moving in, book a demo to see the subscription and allocation workflow for a multi-investor SPV run end to end.

About the author: Kristina Stark is Growth Manager at ONINO, leading marketing, content, and sales across the German and UK markets. Her work focuses on educating on tokenization infrastructure, regulated digital issuance, and how European issuers reach retail investors under MiFID II, PRIIPs, and the EU Listing Act. Kristina studied Business Management and Digital Innovation & Entrepreneurship at City, University of London. LinkedIn: linkedin.com/in/kristina-stark-1b760b1bb.

This article is for general information only and does not constitute legal advice.

Last reviewed by Lukas Wipf CPO & Co-Founder at ONINO, 26 June 2026.

Want to learn more how this can be applied to your business?

Read related Articles

Capital allocation in private markets: why it stays inefficient and how shared infrastructure speeds allocation and widens investor participation