Regulation

How to Launch a Crowdfunding Platform in Europe Under ECSPR (2026 Guide)

A practical 2026 guide to launching an ECSPR crowdfunding platform: licence, EUR 5M cap, capital, KIIS, EU passport, jurisdictions and costs

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Under ECSPR (Regulation (EU) 2020/1503), one licence lets a crowdfunding platform run investment-based and lending-based offers across the entire EEA, with passporting into new member states just 15 days after notification. Core requirements: own funds of EUR 25,000 or 25% of fixed overheads, a EUR 5 million per-project-owner cap over any 12 months, and a max six-page KIIS per offer. Statutory approval takes three months, realistically six to nine depending on jurisdiction. The biggest cost and timeline levers are software and time-to-authorisation, which is where build-vs-buy matters most.

Launching a crowdfunding platform in Europe used to mean navigating a different rulebook in every country. Since November 2021, one regulation has replaced that patchwork:

The European Crowdfunding Service Providers Regulation, or ECSPR (Regulation (EU) 2020/1503). Get authorised once, and you can serve project owners and investors across the entire European Economic Area (EEA).

This guide covers the full path from decision to go-live. It explains what the licence actually authorises, the requirements that decide whether you qualify, how the authorisation process works and where to apply, what it costs, and how to choose the platform software that will run day to day. If you are deciding whether to build this yourself or buy existing infrastructure, the later sections are written to aid you in this decision.

What an ECSPR Licence Lets You Do

A Crowdfunding Service Provider licence is a single EU authorisation that lets a platform match investors with businesses raising capital, anywhere in the EEA, under one set of rules. It covers two business models on the same licence.

First is investment-based crowdfunding, where the platform allows the placement of transferable securities such as equity or bonds. The closest traditional comparison is a private placement venue.

Second is lending-based crowdfunding, where the platform matches investors who lend with project owners who borrow. The platform itself neither lends nor borrows; it intermediates, and it may offer portfolio management of individual loan portfolios.

What an ECSPR Licence Doesn’t Let You Do

It is equally important to understand what falls outside ECSPR. The regulation is scoped to business finance, so reward-based crowdfunding, donation-based fundraising, and consumer lending are all out of scope - Reward-based crowdfunding exchanges money for a product or perk (not a financial return), and donation-based fundraising involves no expected return at all - so neither creates a security or loan for ECSPR to regulate. Consumer lending does involve a loan, but it's personal borrowing rather than business finance, so it falls under separate consumer credit rules instead.

On the digital-asset question, the line is drawn by instrument type: where an instrument qualifies as a financial instrument under MiFID II and is offered through a crowdfunding platform, it sits inside ECSPR; crypto-assets governed by MiCA sit outside it and require a separate authorisation - which would be handled by the issuers independently. Knowing which regime applies before you design your offering saves considerable time and paper later.

Do You Need an ECSPR Licence? The Core Requirements

If you intend to operate a platform that facilitates business investment or lending offers to the public across the EU, then yes, you need to be authorised by a national competent authority. The transitional period for pre-existing national platforms ended on 10 November 2023, so operating in scope without a licence is no longer an option. Before starting the application, it is worth understanding the four requirements that most often determine whether a business qualifies and how it should be structured.

Requirement | What ECSPR sets |

|---|---|

Regulatory capital | The higher of EUR 25,000 or one quarter of the prior year's fixed overheads (Article 11) |

Per-project funding cap | EUR 5 million per project owner over any rolling 12-month period |

Investor disclosure | Key Investment Information Sheet (KIIS), up to six pages, per offer |

EU passport | Services can start in a new member state 15 days after notification (Article 18) |

The EUR 5 Million Per-Project Threshold

ECSPR caps each project owner at EUR 5 million raised over any 12-month period, counted across all crowdfunding platforms combined.

The cap attaches to the project owner, not to your platform, and it is measured at the moment a new offer launches. If a business needs to raise more than that in a year, the offer moves into the prospectus regime under Regulation (EU) 2017/1129 and leaves ECSPR scope entirely. Your platform cannot self-issue a prospectus, so the practical options are to pause a raise at the threshold or to work alongside a MiFID investment firm for larger tickets. Because you carry the responsibility to verify the cap rather than simply trust a declaration, this check needs to be built into your onboarding from day one.

Capital: EUR 25,000 or a Quarter of Operating Costs

The prudential requirement is deliberately light compared with a MiFID firm. You must hold own funds equal to the higher of EUR 25,000 or 25 percent of the previous year's fixed overheads. The requirement can also be met, wholly or partly, by an insurance policy or a bank guarantee for the same amount, although in practice most operators simply hold the capital because insurance tends to price to a similar annual cost. Most platforms carry a buffer above the floor so that a growing cost base does not force a mid-year top-up.

Sophisticated vs Non-Sophisticated Investors, and the KIIS

ECSPR sorts investors into two tiers and applies stronger protections to the retail majority.

Dimension | Sophisticated investor | Non-sophisticated investor |

|---|---|---|

Definition | Meets MiFID II professional criteria, or self-certifies against income, net-worth, and experience tests | Any investor who is not sophisticated; the default for retail |

Onboarding | Lighter procedural steps | Entry knowledge test, loss simulation, and investment limits |

Reflection period | Not required | Four-day pre-contractual reflection period |

Warning trigger | None specified | Above the greater of EUR 1,000 or 5 percent of net worth |

Every offer must be accompanied by a Key Investment Information Sheet, the ECSPR equivalent of a prospectus summary. It runs to a maximum of 6-pages in a standardised format, it is produced per project (or at platform level for a lending pool), and it must be displayed before an investment is made. The project owner drafts the KIIS and bears primary responsibility for its content, while your platform is responsible for vetting it for completeness and clarity under ESMA technical standards. Incomplete or misleading KIIS documents have been among the most common supervisory findings since the regime began, so treat the KIIS workflow as a core product feature, not an afterthought.

How to Get an ECSPR Licence, Step by Step

Article 12 sets the authorisation procedure, and every national competent authority applies it in broadly the same way. The file is heavier than a simple payment-service registration but lighter than a full MiFID application. In practical terms, the submission needs to cover the following.

A programme of operations setting out whether you offer investment-based, lending-based, or both, plus target markets, project-owner sectors, investor types, revenue model, and fee structure.

A 3-year business plan with internally consistent projections, governance arrangements with at least two people effectively running the business, and a conflicts-of-interest policy.

Internal procedures for project-owner due diligence, risk assessment, default and exit disclosures for lending, complaints handling, outsourcing, and record-keeping.

ICT and security documentation aligned with DORA, which has applied to crowdfunding providers as financial entities since 17 January 2025.

Evidence of capital, plus fit-and-proper questionnaires for management and for any shareholder holding 20 percent or more.

The statutory clock is three months from a complete file, but real-world timelines run longer once you account for back-and-forth with the regulator, typically six to nine months. Where you apply matters, both for speed and for supervisory culture.

Jurisdiction | Authority | Typical timeline | Notes |

|---|---|---|---|

Lithuania | Bank of Lithuania | 3 to 5 months | English-language process, large passported population |

Estonia | Finantsinspektsioon | 3 to 6 months | Digital-first, strong fit for tech-led platforms |

Germany | BaFin | 6 to 9 months | Thorough process, deep domestic market |

France | AMF | 6 to 9 months | Deep domestic crowdfunding market, high-quality supervision |

Spain | CNMV | 6 to 9 months | Largest retail crowdfunding investor base, process in Spanish |

Italy | CONSOB | 6 to 12 months | Large lending market, longer for complex platforms |

Practical implications:

If you're outside the EU/EEA entirely, you'd need to establish a subsidiary or entity within a member state first - you can't apply directly from a non-EU country.

If you're already in the EU/EEA but in a country not on this list (or with a slower regulator), you can still choose to set up your licensed entity in Lithuania, Estonia, etc. Rather than your home country.

The tradeoff is usually: faster/cheaper jurisdictions vs. wanting a domestic presence and reputation in a specific market (e.g., licensing in France if France is your primary target market for credibility reasons).

Once authorised in your chosen member state, the single-licence passport under Article 18 lets you expand without a new application. You notify your home authority of the state you intend to serve, and you can begin the process 15-days later. Host states cannot re-authorise you, demand additional capital, or reapply their national disclosure rules, though language, marketing, and tax rules remain local. That passport is the main reason founders choose this regime rather than a national one, and it is why a platform authorised in Lithuania or Estonia can serve project owners and investors in Germany, France, or Spain. For a German operator, the practical trade-off is licensing at home with BaFin, which sits closest to your market but runs a longer process, or authorising faster in Lithuania or Estonia and passporting into Germany.

That trade-off exists because authorisation speed varies enormously from one national regulator to the next, even though ECSPR sets the same three-month statutory clock for all of them. Karsten Wenzlaff, who helped shape the regulation, has seen the gap first-hand:

Expert Quote:

"Their regulator was able to process these license applications within six weeks... And in other countries it took them sometimes 18 months because they were going back to the platform, asking for more information and then would drag this process along."

Secretary General, German Crowdfunding Association, Board Member EDFA

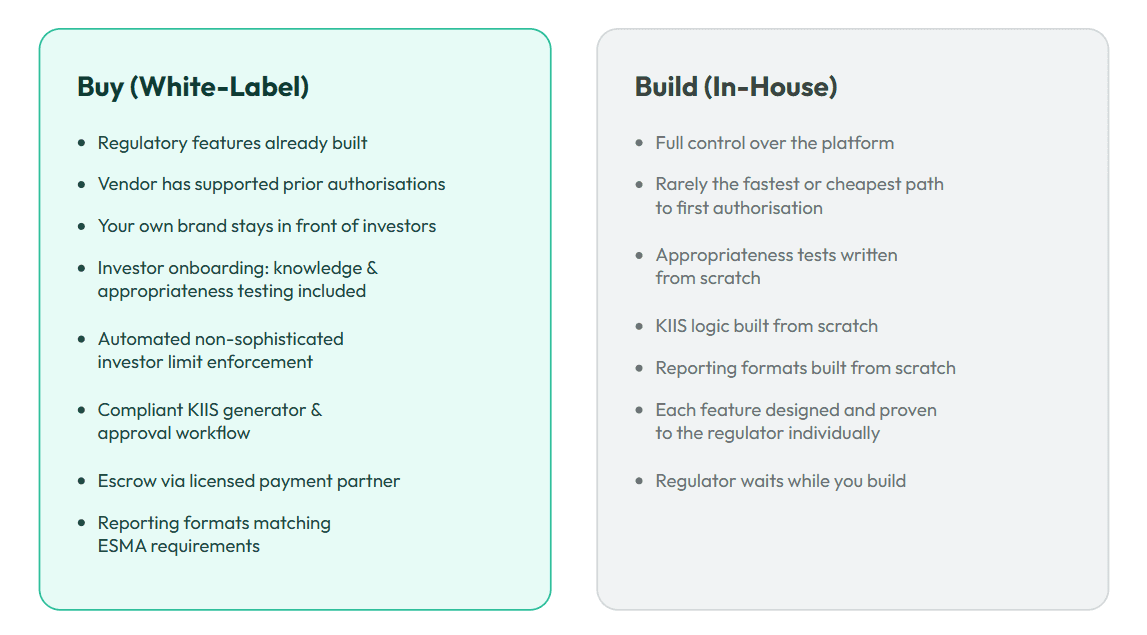

Crowdfunding Platform Software: Build vs Buy

The licence is the legal layer. The platform is the operational layer, and it is where most of the real work sits: investor onboarding, project-owner due diligence, the KIIS workflow, investment flows, payments and escrow, an investor dashboard, and regulatory reporting. There are three broad routes to that software, and the right one depends on your timeline, budget, and how much regulatory logic you want to own.

Building in-house gives you full control but is rarely the fastest or cheapest path to a first authorisation, because you are effectively writing the appropriateness tests, KIIS logic, and reporting formats from scratch while the regulator waits. Open-source crowdfunding software lowers the licensing cost of the codebase, but it shifts the compliance burden entirely onto your team, and generic templates seldom encode ECSPR-specific requirements such as investor-tier limits or the reflection period. White-label crowdfunding platform software suits operators who want to reach go-live in a defined timeframe, because the regulatory features are already built, the vendor has typically supported prior authorisations, and you keep your own brand in front of investors.

Buying proven infrastructure means the compliance surface is already built rather than something you assemble under regulatory deadline pressure. That surface includes investor onboarding with knowledge and appropriateness testing, automated enforcement of non-sophisticated investment limits, a compliant KIIS generator and approval workflow, escrow or segregated handling of investor funds through a licensed payment partner, and reporting formats that match ESMA requirements. Unlike a from-scratch build, where each of these has to be designed, tested, and proven to a regulator one at a time, a mature white-label platform arrives with them already validated across prior authorisations, so the regulator is reviewing a known quantity rather than an unproven system. This is precisely the calculation ONINO's white-label investment infrastructure is built to remove: the regulated workflow ships ready to demonstrate, from day one of your application, rather than becoming a dependency your authorisation timeline has to wait on.

How Much Does It Cost to Launch a Crowdfunding Platform?

There is no single sticker price, but the cost of launching an ECSPR platform breaks into predictable components, and modelling them early prevents unpleasant surprises during authorisation. The indicative ranges below vary by jurisdiction and scope and should be validated with your advisers.

Regulatory capital: the EUR 25,000 floor or 25 percent of projected fixed overheads, held as own funds.

Licensing and legal: advisory support for the Article 12 file, legal structuring, and fit-and-proper documentation, indicatively in the region of EUR 30,000 to EUR 100,000 depending on jurisdiction and complexity.

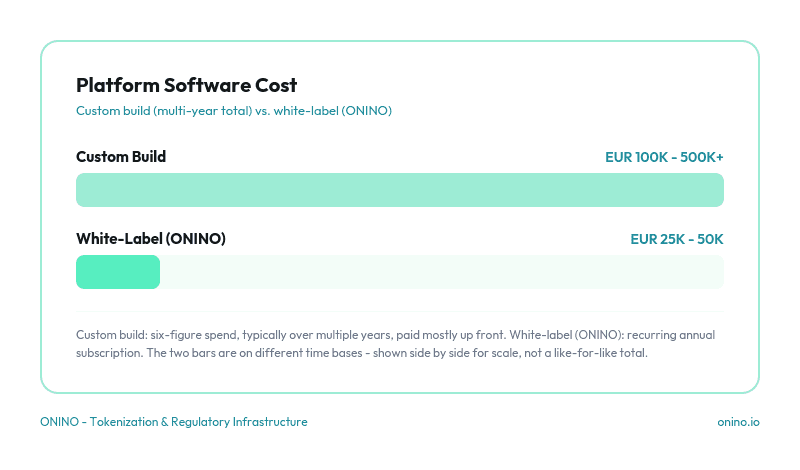

Platform software: the largest variable, from a six-figure multi-year spend for a custom build to a white-label subscription commonly in the low-to-mid five figures per year.

Payments and escrow: integration with a licensed payment or e-money partner to hold and settle investor funds.

Ongoing compliance: DORA-aligned ICT controls, audits, reporting, and staff time, which recur every year.

The strategic point is that the two largest line items, software and time-to-authorisation, are also the two you can most directly influence by your build-versus-buy decision. Proven infrastructure compresses both, which is why the total cost of a bought platform is often lower than a build once the delay in revenue is priced in.

Platform Types and Use Cases

ECSPR is broad enough to support several distinct platform models, and the requirements above apply across all of them.

Equity crowdfunding platforms facilitate investment into company shares and are a natural fit for angel networks and investor clubs formalising deal flow that has outgrown spreadsheets and email.

Lending-based platforms match investors with businesses borrowing for a defined purpose and carry the additional obligations around credit-risk disclosure and default management.

Real estate crowdfunding platforms, popular across the DACH region, let developers raise project capital from a base of private investors, and they benefit most from infrastructure that can be reused across a pipeline rather than rebuilt for every project.

Across all of these, the operators who scale are the ones who treat investor management as reusable infrastructure. A platform built for investor clubs and networks turns a growing community into a repeatable, auditable process, and the same logic applies to private markets operators running multiple raises in parallel.

Beyond the Licence: Investor Operations That Scale

Capital isn't what caps a platform's growth - investor operations are. Fragmented onboarding, manual subscription documents, and reporting rebuilt for every round will limit your volume long before your deal flow does, and these are exactly the gaps a regulator probes during due diligence.

Well-designed infrastructure standardises subscription and documentation, maintains a central and auditable investor record, and supports digital subscription and transfer records where later transferability becomes relevant. That auditability is not a nice-to-have. It is the difference between a supervisory review that takes days and one that takes weeks, and it compounds in value as your portfolio of offers grows. Building this foundation once, and reusing it across every raise, is what separates a platform that scales from a series of one-off campaigns.

Launch Faster With Regulated Infrastructure

Authorisation and technology are two halves of the same launch. The licence proves you can operate; the platform proves you can operate at scale without the operational drag that stalls most new entrants. ONINO provides the white-label investment infrastructure that sits underneath a compliant crowdfunding platform, from onboarding and subscription through to a central investor record, so your team can focus on deal flow and regulatory strategy rather than rebuilding the plumbing. If you are scoping a launch, book a demo to see how the pieces fit your model.

About the author

Kristina Stark is Growth Manager at ONINO, leading marketing, content, and sales across the German and UK markets. Her work focuses on educating on tokenization infrastructure, regulated digital issuance, and how European issuers reach retail investors under MiCAR, MiFID II, PRIIPs, and the EU Listing Act. Kristina studied Business Management and Digital Innovation & Entrepreneurship at City, University of London. LinkedIn: linkedin.com/in/kristina-stark-1b760b1bb.

Want to learn more how this can be applied to your business?

Read related Articles

A practical 2026 guide to launching an ECSPR crowdfunding platform: licence, EUR 5M cap, capital, KIIS, EU passport, jurisdictions and costs