Regulation

What Is a Tied Agent Under MiFID II?

What a tied agent is under MiFID II Article 29, who is liable, how registration works, typical timelines and costs, and when a tied-agent arrangement fits better than your own licence.

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Key Takeaways

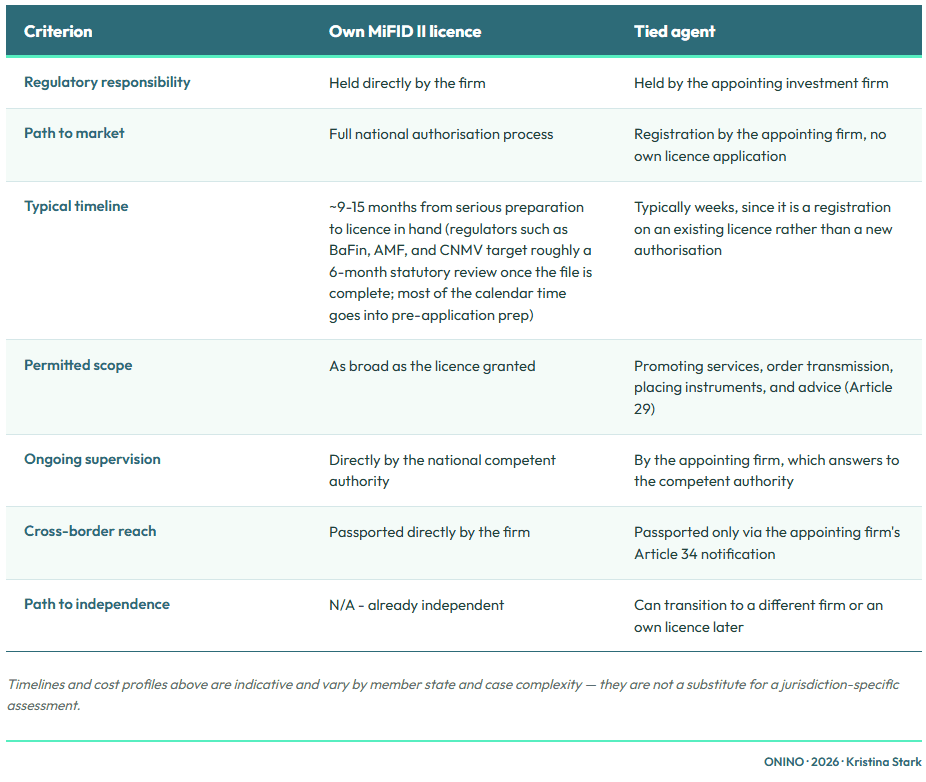

A tied agent is a firm or person who promotes an investment firm's services, receives and transmits client orders, places financial instruments, or gives advice on them - acting under the full and unconditional responsibility of only one appointing investment firm, without holding its own MiFID II licence. Article 29 of MiFID II (Directive 2014/65/EU) requires EU member states to allow this arrangement. The appointing firm remains fully liable, must vet the agent's good repute and competence, and must ensure the agent is entered in a public register - run at national level, not by ESMA. Registration itself is typically a matter of weeks; building an own licence realistically takes 9-15 months.

What Is a Tied Agent Under MiFID II?

A tied agent is a natural or legal person who promotes an investment firm's services, receives and transmits client orders, places financial instruments, or provides advice on those instruments - acting exclusively on behalf of, and under unconditional responsibility of, one investment firm. The concept is defined in Article 29 of MiFID II (Directive 2014/65/EU), which requires every EU member state to allow investment firms to appoint tied agents. A tied agent does not need its own MiFID II investment-firm licence for these activities, because the appointing firm carries the regulatory responsibility on the tied agent's behalf.

In simple words - a tied agent is a person or company that acts as a sales and support arm for an investment firm. They can promote the firm's services, pass along client orders, help sell financial products, or give advice about them - but always on behalf of one firm, and that firm takes full responsibility for whatever the agent does.

Because the main firm is on the hook for them, the tied agent doesn't need to get their own license to do this work. EU law requires every member country to let investment firms use agents this way.

Why are tied agents needed?

Cheaper local presence. Instead of setting up a licensed office in every town or country, a firm can partner with a local person or company who already knows the market and has client relationships.

Faster market entry. Appointing an agent is quicker than building out a regulated branch, so firms can expand into new regions or customer segments faster.

What Does Article 29 of MiFID II Actually Allow a Tied Agent to Do?

Article 29 permits a tied agent to carry out 4 activities on behalf of its appointing investment firm:

Promoting the firm's investment and ancillary services

Soliciting business or receiving and transmitting client orders

Placing financial instruments

Providing advice on those instruments and services

This is a closed list - a tied agent acts strictly within the scope the appointing firm has authorised, and only for that one firm. Member states may also allow a tied agent to hold client money or financial instruments, but only under the appointing firm's full responsibility.

Who Is Liable When a Tied Agent Acts on a Firm's Behalf?

The appointing investment firm is fully and unconditionally liable for any action or omission by its tied agent when the agent acts on the firm's behalf. Article 29(2) requires the firm to ensure the tied agent discloses its capacity and which firm it represents before dealing with any client, and to monitor the tied agent's activities on an ongoing basis to confirm continued compliance with MiFID II. If a tied agent breaches its obligations, the regulatory and civil exposure falls on the appointing firm, not the agent personally - which is exactly why firms vet and monitor agents as closely as they would an internal sales team.

"An Investment firm, or a credit institution, which decides to employ a tied agent, remains fully and unconditionally responsible for any action or omission on the part of the tied agent when acting on its behalf."

*Ioannis Michalaki, Cyprus financial-services lawyer*

How Are Tied Agents Registered and Vetted?

A tied agent must be entered in a public register before an investment firm may appoint it. Article 29(3) requires this register to exist in the member state where the tied agent is established, but the register is run at national level - there is no single EU-wide or ESMA-operated register of tied agents. ESMA's role is limited to publishing links to the national registers that member states maintain. Before registration, the tied agent must be shown to be of sufficiently good repute and to possess the general, commercial, and professional knowledge needed to deliver the service. Because the tied agent rides on the appointing firm's existing authorisation rather than applying for a new one, the registration step itself is typically measured in weeks rather than months - the appointing firm enters the agent's details directly into the national register (for example, via BaFin's electronic system in Germany) once its own due-diligence file is complete.

Can a Tied Agent Operate Across EU Member States?

A tied agent established in an investment firm's home member state can be used to provide services into another member state, but the mechanism sits in Article 34 of MiFID II, not in Article 29 itself. The investment firm notifies its home competent authority of its intention to use tied agents in another member state; the home authority forwards that information to the host member state's competent authority, which publishes it; only then may the firm start providing services there through those agents.

This step is easy to underestimate for distribution partners planning a multi-country capital raise: the tied agent's registration in its home state does not automatically travel with it, and starting to solicit clients in a second country before the host authority has published the notification exposes the appointing firm to acting without proper passporting - a gap regulators have flagged explicitly in ESMA's 2022 supervisory briefing on tied agents.

Own MiFID II Licence or Tied Agent - Which Fits Your Business?

An own licence gives full control over scope and supervision but requires the full authorisation process with your national competent authority. A tied-agent arrangement gets a firm to market faster within a fixed set of activities, in exchange for operating under another firm's full liability and oversight.

Tied Agent vs. Own Licence: A Worked Example

It helps to see the three routes side by side through a concrete case. Take a hypothetical independent wealth adviser in Germany who wants to place fund interests and give investment advice without running its own balance sheet through a full licence application.

Route 1 - Tied agent under Article 29. The adviser signs on as a tied agent of an existing MiFID II-licensed firm. The appointing firm registers it with BaFin, vets its staff for good repute and competence, and takes full liability for its conduct. The adviser can be trading within weeks of completing due diligence, but it is limited to the four Article 29 activities and cannot hold itself out as independently licensed.

Route 3 - Own MiFID II licence. The adviser applies directly to BaFin. Realistically, that means 9-15 months of preparation and review, its own governance, capital, and compliance infrastructure, and full control over the services it offers and the markets it serves. Liability sits with the firm itself from day one.

The decision driver is rarely the timeline alone - it is who carries liability and capital requirements. Route 1 trades independence for speed and a lighter capital burden, because the umbrella or appointing firm absorbs the regulatory risk. Route 2 trades a longer runway for full control and no dependency on another firm's risk appetite. Firms that expect to outgrow a tied-agent or liability umbrella arrangement within a year or two often plan the own-licence route from the outset, using white-label infrastructure to build the operational stack while the licence application is in progress.

Who Actually Needs a Tied Agent Arrangement?

In practice, three groups use the tied-agent route: independent wealth managers and advisers who want to distribute or advise on investments without becoming a licensed investment firm themselves; distribution partners placing securities or fund interests as part of a capital raise; and fintech founders who want to test a regulated distribution channel before committing to a full licence application. For issuers raising capital through structures such as SPVs, the tied-agent question matters directly: whoever places the securities with investors must either hold its own licence or act as a tied agent of a firm that does - a point asset managers evaluating a distribution route should settle early.

The ONINO Licence-or-Liability Test

Scope question: Does the fixed list of promotion, order transmission, placement, and advice actually cover the full business model?

Liability question: Is the business prepared to operate under another firm's full regulatory responsibility?

Exit question: How realistic, and how costly, is a later move to an own licence?

A firm that answers all three in favour of speed and simplicity is usually well served by a tied-agent arrangement. A firm that needs control over its own compliance infrastructure, expects to scale beyond the Article 29 activity list, or cannot accept sitting under another firm's risk appetite should plan the own-licence route early - for example by using white-label infrastructure that handles the operational build while regulatory responsibility stays with the firm itself. Neither path is inherently better: a tied-agent arrangement that outgrows its scope within a year is a false economy, and an own licence built for a business model that never needs its full breadth is over-engineering.

For background on related structures, see our FAQ and About pages. For the Germany-specific version of this model, including the KWG and WpIG framework, see our companion post on the German liability umbrella

If you're weighing a tied-agent arrangement against building toward your own licence, book a demo with ONINO to talk through your distribution structure.

Not ready for a full conversation yet? Start with our FAQ to see how tied-agent and licensing questions come up for other firms.

About the author: Kristina Stark is Growth Manager at ONINO, leading marketing, content, and sales across the German and UK markets. Her work focuses on educating on tokenization infrastructure, regulated digital issuance, and how European issuers reach retail investors under MiCAR, MiFID II, PRIIPs, and the EU Listing Act. Kristina studied Business Management and Digital Innovation & Entrepreneurship at City, University of London. LinkedIn: linkedin.com/in/kristina-stark-1b760b1bb.

This article is for general information only and does not constitute legal advice.

Last reviewed by Lukas Wipf CPO & Co-Founder at ONINO, 26 June 2026.

Want to learn more how this can be applied to your business?

Read related Articles

What a tied agent is under MiFID II Article 29, who is liable, how registration works, typical timelines and costs, and when a tied-agent arrangement fits better than your own licence.