News

Stuck Between Bank and VC: Why Mid-Sized Real Estate Issuers Can't Get Funded, Based on a 250-Issuer Cohort Analysis

Why can't mid-sized European real estate get funded? A 250-issuer cohort analysis of the financing gap and the digital securities path out

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Mid-sized European real estate deals in the €2M to €20M band fall into a structural financing gap: too small for institutional funds (which target €25M+ tickets and 15-20% IRR) and too capital-costly for banks under Basel III/IV. Across a 250-issuer cohort, more than two-thirds of mid-market deals reviewed ended up repriced down, restructured into a larger combined deal, or shelved entirely, despite sound underwriting. Digital securities infrastructure is the only path that fixes both sides of the gap at once: issuers raise from 50-500 investors under EU prospectus exemptions, and minimum tickets drop from €100,000 in traditional direct real estate to €500-1,000 in tokenized real estate, a 99% reduction that opens the asset class to a far wider investor base.

Stuck Between Bank and VC: Why Mid-Sized Real Estate Issuers Can't Get Funded, Based on a 250-Issuer Cohort Analysis

The mid-market real estate financing gap in Europe has a defined shape. It is not a vague complaint about "tight credit markets." It is a structural band - roughly €2M to €20M in total deal size - where two well-developed funding paths exist on either side, and neither covers the middle.

Below €2M, a developer or asset manager can usually finance through Sparkasse, Volksbank, or local bank credit, often layered with personal guarantees or family equity. Above €20M, institutional debt funds, life-insurance balance sheets, and large-ticket private equity become viable counterparties. In between sits the operational core of European real estate: residential value-add projects, mixed-use redevelopment, hotel and serviced-apartment financing, smaller commercial assets, and energy-efficient retrofits that require capex stacks not standard mortgages.

Why banks pass

The bank-side answer is rarely "your deal is bad." It is more often a stack of capital-cost, regulatory, and operational reasons that combine to make a mid-sized real estate deal uneconomic for the lender's balance sheet.

Capital cost under Basel III / IV. Real estate exposure carries a specific capital weighting that, for non-prime collateral or higher-LTV positions, can push the required regulatory capital well above what the deal's interest margin will return. For a €5M deal at standard mid-market spreads, the after-capital return often does not clear the bank's internal hurdle.

LTV ceilings that mid-market deals routinely brush. Banks underwrite to conservative LTVs on residential and mixed-use collateral. A value-add deal that requires 65-75% leverage to make sponsor economics work is structurally outside many banks' standard sheet - even when the underlying NOI projections are sound.

Reduced SME credit appetite since 2022. Across the cohort, post-2022 credit committees applied notably tighter review standards to mid-sized real estate exposures, particularly residential development. This is consistent with broader ECB lending data showing tightening in real estate exposure across the eurozone.

The unit economics of relationship lending. A €5M deal carries the same legal, KYC, and credit-committee cost as a €50M deal - but generates a tenth of the fee revenue. For all but the most relationship-driven local banks, the deal simply does not pay back the diligence overhead.

The deal can be sound. The structural answer is still no.

Why VC and PE pass

Venture capital does not finance real estate at all. The asset class returns 6-12% over multi-year holds, while VC mandates target 25%+ IRR on companies that can theoretically return 10-100×. Real estate's risk-return profile is the structural opposite of VC's. This is not a fixable mismatch - it is a definitional one.

Private equity and institutional real estate funds do finance the asset class, but they pass on the €2M-€20M band for different structural reasons:

Return profile mismatch. Most institutional real estate funds target 15-20% IRR on value-add strategies or 8-12% on core-plus. Mid-market deals can produce these returns at the asset level, but the cost of running a small deal through an institutional vehicle - legal, due diligence, ongoing asset management - erodes net IRR to where the fund's underwriting hurdle no longer clears.

Ticket-size economics. A €100M closed-end fund deploying into 6-10 deals does not look at €5M positions. The diligence cost is the same as a €50M position; the fund's allocation strategy doesn't accommodate the small ticket; the GP's economics push toward larger deals.

Timeline mismatch. Mid-market deals often need committed capital in 4-8 weeks to compete on the sell side. Institutional fund processes - IC approval, fund-of-fund LP look-through, legal subscription docs - typically run 8-16 weeks for new commitments. By the time the institutional process closes, the deal has moved.

Mandate fit. Institutional capital concentrates in prime commercial, large residential portfolios, and core logistics. A €5M residential value-add deal in a tier-2 German city is operationally interesting but mandates-out for most institutional vehicles.

The deal can be sound. The structural answer is still no.

The cost of the gap

The financing gap has direct, quantifiable cost - to issuers, to investors, and to the broader real estate economy.

To issuers. Across the cohort, projects in the gap typically end in one of three places: they get repriced at a worse valuation (developer absorbs a 10-20% haircut to fit a bank's smaller LTV envelope); they get restructured into a larger combined deal that takes 6-12 months to assemble; or they get shelved entirely. Each outcome carries opportunity cost - delayed delivery, lost market window, eroded sponsor returns.

To investors. The gap simultaneously cuts off retail and affluent investors from the asset class. Mid-market real estate has historically produced more risk-adjusted return than core commercial precisely because the institutional crowd does not touch it. Closing the supply-side of the gap (issuer-side) without addressing the demand-side (investor-side) only relocates the problem.

To housing and urban supply. Residential redevelopment, value-add, and energy-efficient retrofits - exactly the asset profile that sits in the gap - is also exactly the asset profile European policy frameworks need more of. The gap is a real-economy bottleneck, not just a financial-markets curiosity.

If this pattern describes a deal you're trying to fund, the structural issue is rarely the deal - it's the path. See how mid-sized real estate raises are structured through digital securities infrastructure.

How digital securities infrastructure changes the funding calculus

The structural exit from the gap is not "find a more flexible bank" or "pitch a different fund." Both paths have rational reasons to pass - those reasons are not going to change. The exit is a third path: digital securities infrastructure that connects mid-sized issuers directly to a wider investor base, under a regulated framework that institutional capital and retail capital can both recognize.

Prospectus exemptions and multi-investor structures (supply side)

EU regulation already allows mid-sized real estate raises without a full prospectus, but only if the structure fits inside specific exemption thresholds. Three regimes matter:

EU Prospectus Regulation small-issuer exemption - up to €8M raise within a 12-month period in many member states (the exact ceiling varies; Germany allows €8M, others lower).

ECSPR (European Crowdfunding Service Provider Regulation) - covers raises up to €5M per 12-month period with a passported license.

eWpG (Gesetz über elektronische Wertpapiere) in Germany - provides a regulated framework for electronic securities, including registered bonds (Schuldverschreibungen), with a BaFin-supervised registry layer.

A mid-sized real estate issuer can structure a €2M-€8M raise inside these exemptions. The technology layer is incidental. The regulatory layer is what makes the raise legal, recognized, and operationally manageable.

The second piece is multi-investor structures. Managing 50 investors through manual spreadsheets, KYC PDFs, and email confirmations breaks down operationally somewhere around 30-40 participants. Managing 200 or 500 is impossible without infrastructure. Digital securities platforms automate the cap table, the distribution payments, the reporting, the secondary transfers, and the regulatory record-keeping - bringing the per-investor operational cost down to where a €500-€5,000 ticket is economically viable for the issuer.

Opening up for more investors

The supply-side fix is meaningless without a demand-side fix. If issuers can raise from many investors but investors can't enter at deal-relevant ticket sizes, the gap stays open. The minimum-ticket shift is the single most visible structural change tokenization delivers:

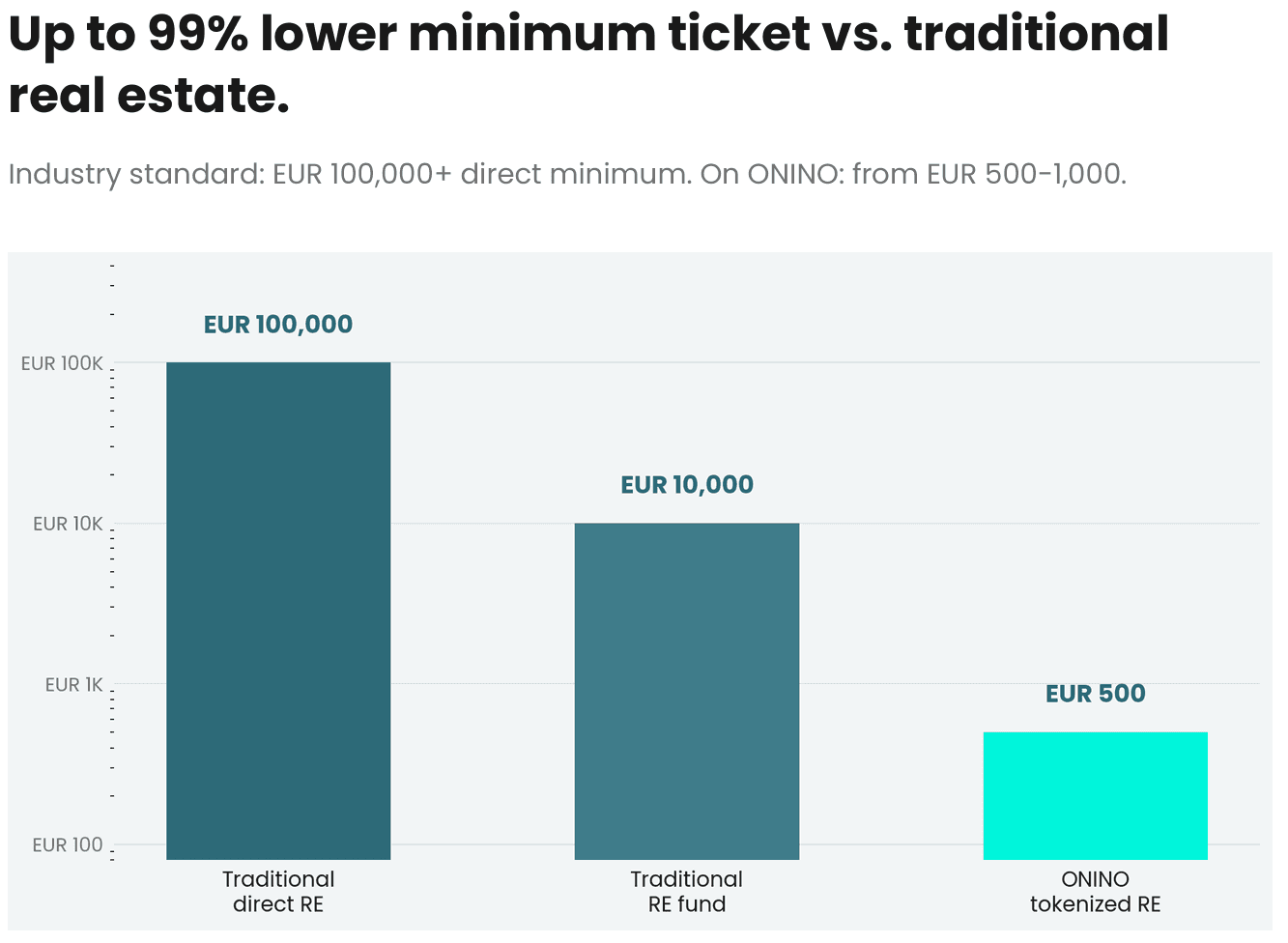

Minimum ticket comparison: Traditional direct RE €100,000 vs. Traditional RE fund €10,000 vs. ONINO tokenized RE €500 - up to 99% lower minimum ticket

Up to 99% lower minimum ticket vs. traditional real estate. Industry standard: EUR 100,000+ direct minimum. On ONINO: from EUR 500-1,000.

Traditional direct real estate co-investment has effectively excluded everyone outside ultra-high-net-worth and institutional family offices. A €100,000 minimum ticket prices out the affluent private investor, the smaller family office, and any pooled member structure. Traditional real estate funds improved access by an order of magnitude to roughly €10,000 - but still gate the long tail of affluent investors and operationally make small allocations expensive.

Tokenized real estate on regulated digital securities infrastructure brings the minimum ticket to €500-€1,000. This is not a marketing claim. It is a function of how the on-chain cap-table layer eliminates the per-investor fixed cost that traditional fund structures inherit from transfer agents, fund admin, and paper-based subscription docs. When fixed cost per investor drops from hundreds of euros to single digits, the floor of a viable allocation drops with it.

This is where ONINO converts the gap into a solution. The platform operates the regulatory infrastructure - eWpG-registered electronic securities under Cashlink as a BaFin-supervised registry, MiFID II classification, integrated KYC/AML at onboarding, ERC-3643 as the on-chain compliance standard. The issuer gets a path to a wider investor base at deal-relevant size. The investor gets access to mid-market real estate at a ticket they can actually allocate. The asset manager or financing consultant structuring the deal gets to deploy a white-label digital securities platform under their own brand, with ONINO holding the regulatory layer underneath.

The structural gap closes from both sides at once. That is what makes digital securities the structural exit - not just a different path.

Why digital securities are not crypto

The most common misread among issuers evaluating this path for the first time: assuming "tokenization" means "crypto." It does not. Digital securities are regulated financial instruments under MiFID II. They have a named issuer, contractually defined rights (interest, principal, dividend, participation), an EU regulatory framework (eWpG in Germany, ECSPR cross-border, AIFMD for fund structures), and registry-grade record-keeping under supervised entities like Cashlink. MiCA - the EU's crypto-asset regulation - explicitly excludes financial instruments already covered by MiFID II. Digital securities sit in the MiFID II perimeter, not the MiCA one. This is the regulatory point that asset managers, banks, and family offices need clear before they will move forward.

Which funding path fits which deal?

The decision matrix below maps the three structural paths against six criteria that determine fit. Use it to identify which path a specific deal belongs in - and where digital securities is the only structurally available option.

Criterion | Bank lending | PE / institutional fund | Digital securities |

|---|---|---|---|

Deal size sweet spot | €10M+ on standard LTV terms | €25M+ ticket per position | €1M-€50M |

Return profile fit | Fixed coupon, 4-8% | 15-20%+ IRR on value-add | Variable, 6-15% blended |

Timeline to close | 4-12 weeks | 6-18 months (IC + LP look-through) | 4-8 weeks post-platform setup |

Investor count | 1 (the lender) | 1-3 LPs | 50-500 retail and affluent investors |

Regulatory path | Bank credit committee | Fund prospectus or AIFMD | EU Prospectus exemption, ECSPR, or eWpG |

Liquidity for investor | None (lender holds to maturity) | 7-10 year fund lockup | Secondary-market transferability via registry |

A second table makes the gap itself visible - the deal profile that gets systematically excluded from the first two columns:

Deal attribute | Why banks pass | Why PE / institutional funds pass |

|---|---|---|

Deal size €2M-€20M | Diligence cost flat across deal sizes; small deals don't pay back the overhead | Below fund ticket-size threshold; allocation strategy concentrates in larger positions |

Equity ratio 20-40% | Higher than standard SME credit profile; pushes LTV outside comfort | Lower than PE control-position requirements |

Residential / mixed-use / value-add asset | Outside LTV comfort for certain collateral types; local-market specialization gap | Not core for institutional mandates (which concentrate in prime commercial and large residential portfolios) |

Standard property mortgage as collateral | Acceptable but Basel capital weighting punishes returns | Insufficient leverage for institutional return targets |

Holding period 2-7 years | Too long for bridge debt; awkward against standard term-sheet conventions | Too short for closed-end PE fund lifecycle |

Read across both tables: the deals in the gap are not bad deals. They are deals whose profile fits neither path's economics.

ONINO's position - and what it does not solve

ONINO operates regulated digital securities infrastructure for issuers in exactly this band. The architecture: eWpG-registered electronic securities with Cashlink as the BaFin-supervised registry, MiFID II-classified instruments where applicable, ERC-3643 (T-REX) as the on-chain compliance standard, integrated KYC/AML at onboarding, and a white-label platform layer that lets asset managers, banks, and structuring consultants deliver the platform under their own brand. Eight live platforms, €35M tokenized capital across them, including real estate raises. The Volksbank partnership provides institutional validation that the architecture is bank-grade - a regulated regional bank serves as both investor and platform partner.

What this does not solve, stated plainly:

Secondary market depth is still developing. Tokenized securities can transfer on-chain under a registered structure, but liquidity at any specific moment depends on counterparty availability. Issuers should not promise investors easy exit; they should structure expectations around the holding period.

Investor risk education is the issuer's responsibility. Lower minimums open the asset class to investors who have not previously held real estate. Under regulated structures, the issuer (or platform operator) is responsible for the suitability and disclosure framework - not the technology layer.

Digital securities are not faster bank credit. If a deal genuinely fits standard bank lending and the issuer has the relationship to access it, that is usually still the path of least resistance. The argument here is for deals that the bank path has structurally excluded.

The structural exit exists, and it works - but it is a different operating model, not a free lunch.

Book a structuring call for your real estate deal

If you're sitting on a €2M-€20M real estate deal that has stalled at credit committee or screened out of institutional funds, the right next step is not another bank conversation. It's a 30-minute structuring call with the ONINO team to map your deal against EU exemption frameworks (Prospectus Regulation, ECSPR, eWpG) and evaluate whether a multi-investor digital securities raise fits your timeline, return profile, and investor base.

What you walk away with: a concrete view of which regulatory pathway fits your deal, what the platform setup looks like (typically 4-8 weeks from term sheet), and a realistic estimate of investor reach at €500-€5,000 tickets. No pitch deck, no marketing material - a working structuring conversation, run by people who have done this across 250+ European real estate issuers, with eight live platforms operating on the stack.

Book a structuring call for your real estate deal →

FAQ

What is the EU prospectus threshold for real estate securities?

The EU Prospectus Regulation allows member states to set a national exemption ceiling for small public offers - up to €8M per 12-month period in Germany (and several other member states), lower in others. Below the national threshold, an issuer can offer securities to the public without producing a full EU prospectus, though a securities information sheet (Wertpapier-Informationsblatt under §4 WpPG in Germany) is typically still required. The ECSPR regime adds a separate cross-border passport for raises up to €5M per 12-month period via licensed crowdfunding service providers. Real estate securities can fit inside any of these depending on structure.

Can a mid-sized real estate developer issue digital securities without a bank?

Yes - and this is one of the structural features of the digital securities path. Under eWpG in Germany, an issuer can issue electronic securities directly, with a regulated registry operator (such as Cashlink) maintaining the registry under BaFin supervision. No bank is required as issuer, paying agent, or distribution party. The issuer may still choose to work with a bank for specific services (paying agent function, escrow, distribution support), but the structural ability to issue is not bank-dependent. ECSPR-based raises through licensed crowdfunding platforms similarly do not require bank involvement.

What investor minimum is typical for tokenized real estate in Germany?

Minimum tickets for tokenized real estate on regulated digital securities platforms in Germany typically start between €500 and €1,000, compared to €100,000+ for traditional direct real estate co-investment and roughly €10,000 for traditional real estate funds. The lower minimum is a structural function of how digital securities infrastructure handles per-investor operational cost - automated KYC, on-chain registry, automated distributions - rather than a marketing choice. Issuers can still set higher minimums where the deal structure or investor type makes that appropriate.

Want to learn more how this can be applied to your business?

Read related Articles

Why can't mid-sized European real estate get funded? A 250-issuer cohort analysis of the financing gap and the digital securities path out