Tutorials

How Do You Carry Out a Self-Issuance (Direct Placement)? A 5-Stage Guide

How to carry out a self-issuance: the five steps from structuring the instrument through EU prospectus filing and KYC/AML onboarding to closing, register and reporting - plus the most common mistakes.

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaways

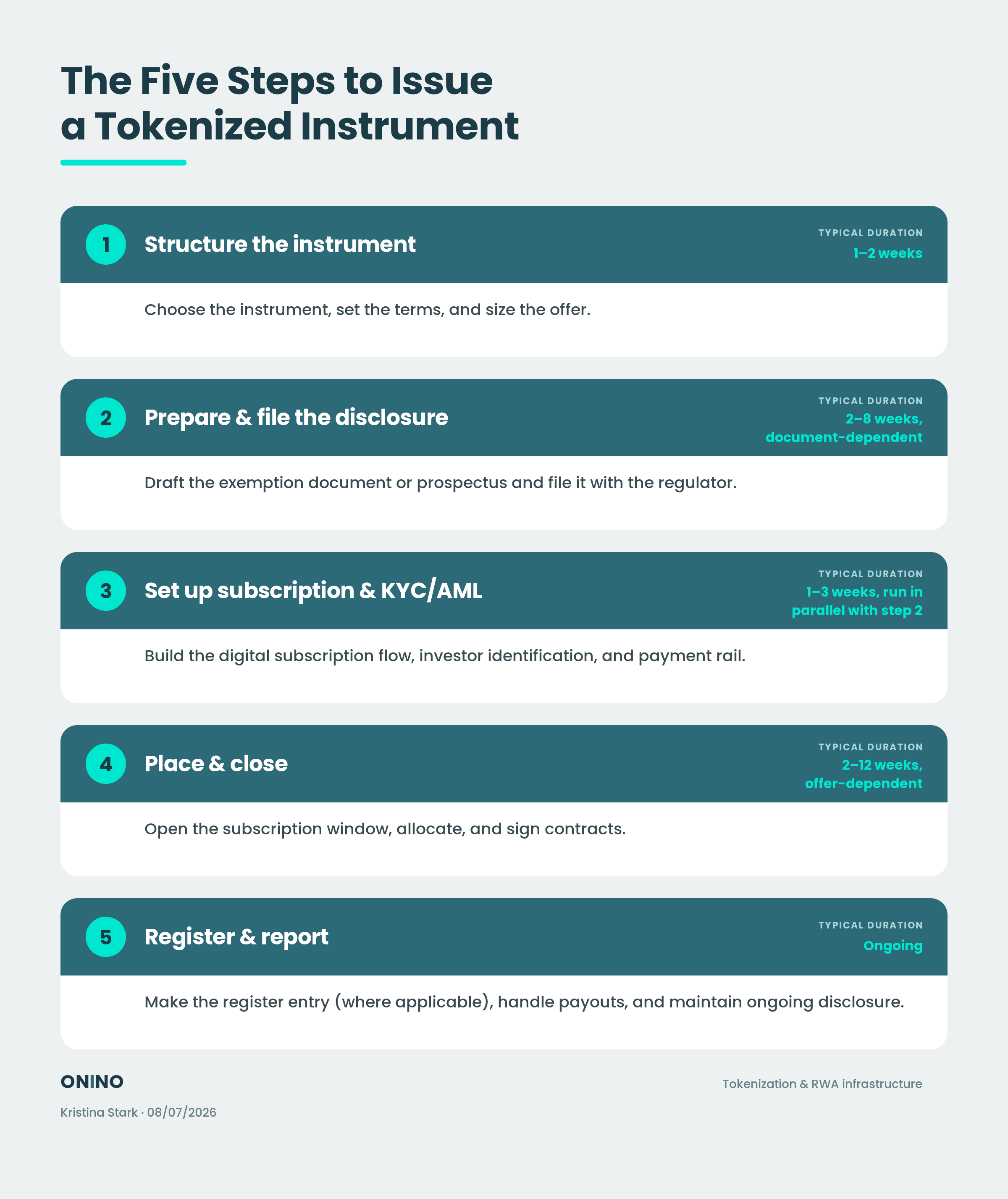

Running a self-issuance process means working through five stages: structuring the instrument, preparing and filing the disclosure document, setting up subscription and KYC/AML onboarding, placing and closing the offer, then registering and reporting afterward. Most issuers lose time on timeline planning and documentation, not on the legal structure itself.

How Do You Carry Out a Self-Issuance (Direct Placement)? A 5-Stage Guide

Running a self-issuance process means working through 5-sequential stages:

Structuring the instrument

Preparing and filing the disclosure document

Setting up subscription and KYC/AML onboarding

Placing and closing the offer

Registering and reporting once the raise is done

What a self-issuance actually is, and how it differs from private placement and crowdfunding, is covered in What Is a Self-Issuance (Direct Placement)?; this post picks up from there and walks through how the process runs in practice, stage by stage, including where issuers most often lose time.

What Are the Five Stages of a Self-Issuance Process?

The process runs as a reusable sequence, followed in the same order regardless of which instrument is used - a bond, subordinated debt, profit-participation right, or a tokenized security. Call it the Direct Placement Runway:

Stage | What happens | Typical duration |

|---|---|---|

1. Structure the instrument | Choose the instrument, set terms, size the offer | 1-2 weeks |

2. Prepare & file the disclosure | Draft the exemption document or prospectus, file with the regulator | 2-8 weeks, document-dependent |

3. Set up subscription & KYC/AML | Digital subscription flow, investor identification, payment rail | 1-3 weeks, run in parallel with step 2 |

4. Place & close | Subscription window, allocation, contract signing | 2-12 weeks, offer-dependent |

5. Register & report | Register entry (where applicable), payouts, ongoing disclosure | ongoing |

The biggest time saving is building stages 2 and 3 in parallel rather than sequentially: the subscription flow doesn't need regulatory clearance to be technically ready, and it can go live the moment the disclosure document clears. Issuers who sequence these two stages instead of running them side by side routinely add several weeks to their time-to-market for no legal reason.

Stage 1: How Do You Structure the Instrument for a Self-Issuance?

Size determines the disclosure route

Size is the term that drives the most downstream consequence, so it has to be fixed with the disclosure route already in view. The reason is that size feeds directly into which disclosure path applies in stage 2: an offer priced just above the de-minimis floor triggers a heavier disclosure obligation than the same offer set just below it. This is why the threshold has to be priced into the offer design upfront rather than discovered later - getting size wrong forces a full rework cycle once the disclosure obligation is reassessed downstream.

Terms determine the subscription rate

The instrument's terms are the other half of what gets locked in at this stage, and they largely determine how well the offer subscribes. Alongside instrument and size, this step fixes the coupon or profit share, maturity, ranking (subordination where relevant), minimum ticket size, and any early-redemption rights. Issuers with an existing investor base from a prior project typically anchor these terms to what that audience already understands, which measurably improves the eventual subscription rate - so setting terms is as much an exercise in reading the investor base as in structuring the capital.

Stage 2: How Do You Prepare and File the Disclosure Document?

Which document you need depends on the exemption route the offer falls under, not on the fact that it's a self-issuance. Under the EU Prospectus Regulation (EU) 2017/1129 - as amended by the EU Listing Act from 5 June 2026 - an offer below €12,000,000 over 12 months needs no EU prospectus. Member states can lower this threshold, but not below €5,000,000. Below the applicable threshold, a lighter national disclosure document usually applies instead; above it, you need a full or EU Growth prospectus. What Is a Self-Issuance (Direct Placement)? covers the exemption ladder in detail - this section picks up once you've chosen a route.

Exemption tier | Disclosure required | Typical review path | Who reviews |

|---|---|---|---|

Below €5M/12mo (harmonised floor) | None (EU-wide) | No regulatory filing | - |

€5M-€12M band (member-state option) | Lighter national document | Filed with the national regulator; completeness review, not a full merits review | National competent authority (e.g. BaFin in Germany) |

Qualified-investor / under-150-persons | None (offer restricted instead) | No regulatory filing; MiFID II classification applied internally | - |

Above the €12M ceiling | Full or EU Growth issuance prospectus | Formal regulatory approval process, passports EU-wide once cleared | National competent authority |

For most issuers, the disclosure-filing stage is a hard gate - not a formality you can rush or work around.

For example, an issuer plans a €4m tokenized bond, announces a launch date six weeks out, and opens marketing. On filing, the regulator doesn't judge the deal - they check the document for completeness and flag two vague risk factors. With no self-certification route, nothing can go live until that's fixed and cleared, which takes four extra weeks. The launch date passes with nothing live and the ready-to-go subscription window sits idle - delay caused purely by committing to a date before clearance.

This matters because it flips where the real risk sits. Teams tend to worry about operational stages like subscription setup, but the binding constraint is regulatory clearance, which they don't control the timing of. Committing to a public launch date beforehand forces every downstream stage to wait on the regulator, turning a manageable review into a bottleneck. The practical takeaway is to treat clearance as a fixed gate and only schedule the launch once it's in hand.

Stage 3: How Do You Set Up Subscription and KYC/AML Onboarding?

Every investor needs to be identified before the contract is concluded, regardless of ticket size, because EU anti-money-laundering rules tie the customer due diligence obligation to the start of the business relationship, not to a euro threshold. Remote identification (video identification or eID) is standard practice across the EU market today.

From 10 July 2027, the EU Anti-Money Laundering Regulation (AMLR) applies directly across all 27 member states, replacing the current patchwork of national transpositions of the AML Directives with one harmonised customer due diligence regime - issuers building a subscription flow now should design it to the stricter, harmonised standard rather than the current national minimum.

Beyond identification, the subscription flow needs to cover: access to the disclosure document before subscription, with documented proof the investor received it; where relevant, MiFID II investor classification (retail, professional, or eligible counterparty); the subscription commitment itself, typically captured through a qualified or advanced electronic signature under the eIDAS Regulation; and payment handling through a connected payment or escrow provider. These elements can be built in parallel with the regulatory filing in stage 2, and KYC records generally need to be retained for several years after the relationship ends - that obligation stays with the issuer even where a third-party provider performs the identification itself.

Stage 4: How Does Placement and Closing Work?

Once the disclosure document is cleared and the subscription flow is live, placement begins: investors get access to the offer, subscribe through the flow built in stage 3, and the issuer accepts subscription commitments - typically in a batch at the end of the subscription window or once a pre-set funding target is reached. From acceptance, the contract is binding, and the platform confirms the subscription, the signed agreement, and the payment receipt digitally.

Where retail investors are involved, a statutory withdrawal window commonly applies after the contract is concluded, during which the subscription isn't yet final. Issuers who communicate the raise as closed - internally or to investors - before that window has run create avoidable rework in how the capital gets deployed.

Stage 5: What Happens After Issuance - Register and Reporting?

For a traditionally-held security, the offer's operational life continues through the issuer's own ongoing administration: coupon or profit payments, investor communication, and statutory record-retention periods. Where the instrument is issued as a tokenized security instead, several EU member states now offer an electronic-register route as an alternative to a paper global certificate - Germany's eWpG is the most established example, under which register entry has constitutive effect: the electronic security legally comes into existence through the register entry itself, not through certificate issuance. Running such a register is itself a licensed activity in the jurisdictions that operate one, which is why most issuers work with a licensed register operator rather than seeking that authorization themselves. Read the eWpG guide for how that specific route works in practice.

4 Common Mistakes When Running a Self-Issuance Process

Timeline sequencing - Setting a subscription launch date before regulatory clearance is granted, then having to push it back.

Documentation gaps - Failing to log proof that the investor received and acknowledged the disclosure document before subscription, leaving that evidence missing if a dispute arises later.

The intermediary question - Paying a third party a fee to place the offer generally changes the regulatory picture. That party typically needs to be licensed, or the issuer needs its own distribution authorization; running an offer through an unlicensed "finder" is a common and avoidable error.

Payment-rail delay - Connecting a payment provider or escrow account only after regulatory filing, even though it can run in parallel with stages 2 and 3.

In practice, the stage that causes delay is rarely one the issuer controls. Across the self-issuances ONINO has supported, structuring, subscription setup and closing move on schedule once a team commits to them - the time gets lost in stage 2, and usually not in drafting the document but in the handoff to whoever reviews or signs off on it.

As ONINO Co-Founder & CPO Lukas Wipf puts it;

"from experience, it always comes down to the fact that they (the third party) don't process things when you say you need it urgently, but when they have time... and that's precisely the link in the chain that falls away with self-issuance.”

Removing it is often the main reason issuers choose self-issuance in the first place: taking that party out of the chain is the one reliable way to get the timeline back under their own control.

Issuers who want to run these five stages on one system, rather than coordinating a separate vendor for each one, can run the whole workflow - subscription, KYC/AML, payments, and, for tokenized instruments, the register - on ONINO's white-label platform, under their own brand and domain. It lets asset managers, banks, and operators launch a compliance-ready financing platform in days and reuse it for every future issuance instead of rebuilding the stack deal by deal.

If you'd rather see how the five stages map onto your specific instrument and jurisdiction, book a demo and the team will walk through how ONINO can help you run your next placement end to end.

About the author:

Kristina Stark is Growth Manager at ONINO, leading marketing, content, and sales across the German and UK markets. Her work focuses on educating on tokenization infrastructure, regulated digital issuance, and how European issuers reach retail investors under MiFID II, PRIIPs, and the EU Listing Act. Kristina studied Business Management and Digital Innovation & Entrepreneurship at City, University of London. LinkedIn: linkedin.com/in/kristina-stark-1b760b1bb.

This article is for general information only and does not constitute legal advice.

Last reviewed by Lukas Wipf CPO & Co-Founder at ONINO, 26 June 2026.

Want to learn more how this can be applied to your business?

Read related Articles

How to carry out a self-issuance: the five steps from structuring the instrument through EU prospectus filing and KYC/AML onboarding to closing, register and reporting - plus the most common mistakes.