Insights

How to Tokenize Invoices and Trade Receivables

Tokenize invoices & trade receivables to unlock working capital faster. Practical guide for SMEs and lenders - covering legal setup, smart contracts & EU compliance.

Lukas Wipf

CPO & Co-Founder

last updated on

Lukas Wipf

CPO & Co-Founder

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Companies waiting 30-90 days for invoice payment can tokenize those receivables into blockchain-based assets, selling them to investors for immediate liquidity. Investors get repaid when the debtor settles the invoice. Unlike traditional factoring (single institution buys the invoice), tokenization enables fractional participation from multiple investors with on-chain transparency. Platforms must verify invoice authenticity and assess debtor credit risk before tokenization, and the legal classification of these tokens varies by jurisdiction.

What invoice tokenization actually is

Tokenizing invoices and trade receivables converts unpaid claims into digital financial instruments that can be financed or traded before the payment date. According to the ECB SAFE survey 2024 (H1), close to half of euro-area SMEs report late payments as a recurring constraint on working capital. The Intrum European Payment Report 2024 puts average European B2B DSO at 56 days. Tokenization is one route to compress that gap and is positioned in the market as a factoring alternative and an invoice discounting alternative.

In legal substance, the token represents an underlying payment obligation that has been packaged as a transferable instrument: in Germany typically the bond security is under the eWpG, in Switzerland a register-uncertificated security under Article 973d OR and the DLT Act. The legal claim sits in a regulated register; the on-chain entry is the canonical transfer mechanism.

That distinction determines who supervises the issuance (BaFin in Germany, FINMA in Switzerland), how the instrument is distributed (MiFID II distribution rules, or the ECSPR carve-out up to €5 million per offer in any 12-month period), and how it is settled on payment (registry redemption by the crypto securities registrar, not a token burn).

Why companies tokenize receivables

Companies need to tokenize receivables because delayed payments create working capital pressure. Especially in supply-chain-driven industries. Manufacturing, logistics, and wholesale. Which carry large receivable balances while still financing production cycles. Tokenizing the delayed payments or debt allows firms to easily split, sell, transfer or manage those debts - providing greater options and financial flexibility.

The EU Federation for the Factoring & Commercial Finance Industry reports EU factoring volume of roughly €2.6 trillion in 2023. Factoring is the dominant solution for SMEs that need to release working capital, which is usually stuck by unpaid invoices. But it carries known limitations: a single financier, opaque pricing, and the requirement to notify buyers in most cross-border arrangements. Tokenization addresses the same working-capital problem with a different structure. Instead of selling a receivable to one factoring company, the issuer packages it as a security and sells it to multiple investors. Pricing reflects the credit risk of the named debtor rather than the seller's bank relationship, and the instrument can be tranched or pooled.

There is a structural advantage to factoring that is often overlooked. Under §354a HGB, German B2B receivables between merchants are assignable even where the underlying commercial contract prohibits assignment. That removes the buyer-consent friction that defines most factoring discussions and is the reason tokenization can run without buyer notification in the German mid-market.

For SMEs and mid-market issuers, the practical effect is a second funding line that runs in parallel with bank financing and traditional factoring, not a replacement for either.

What asset managers and investor clubs gain

The receivables-financing argument is usually told from the issuer's side. From the financier's side, tokenized receivables introduce an asset profile that has historically been locked inside dedicated factoring desks. Three operational properties matter for asset managers and investor clubs.

The first is short, predictable duration. A typical receivable matures in 30 to 90 days. For an allocator holding longer-duration private credit positions, this is a way to add liquid, short-cycle exposure to the real economy without secondary-market dependency.

The second is per-invoice transparency. Each token represents an individually verifiable claim against a named debtor. Underwriting moves from pool-level statistical risk to per-position credit assessment, which fits the diligence workflow asset managers already run on private credit.

The third is automated repayment. Smart-contract logic against the eWpG registry removes the operational drag of collecting and reconciling small-ticket repayments across dozens of invoices.

For asset managers running co-investment vehicles, family offices, and investor clubs syndicating to members, tokenized receivables function as a scalable short-duration sleeve. The token can be held directly by a qualified custodian, wrapped into an AIF or ELTIF 2.0 structure for retail distribution, or held by an existing special fund. Repayments flow back through the same custody endpoint without bilateral integration.

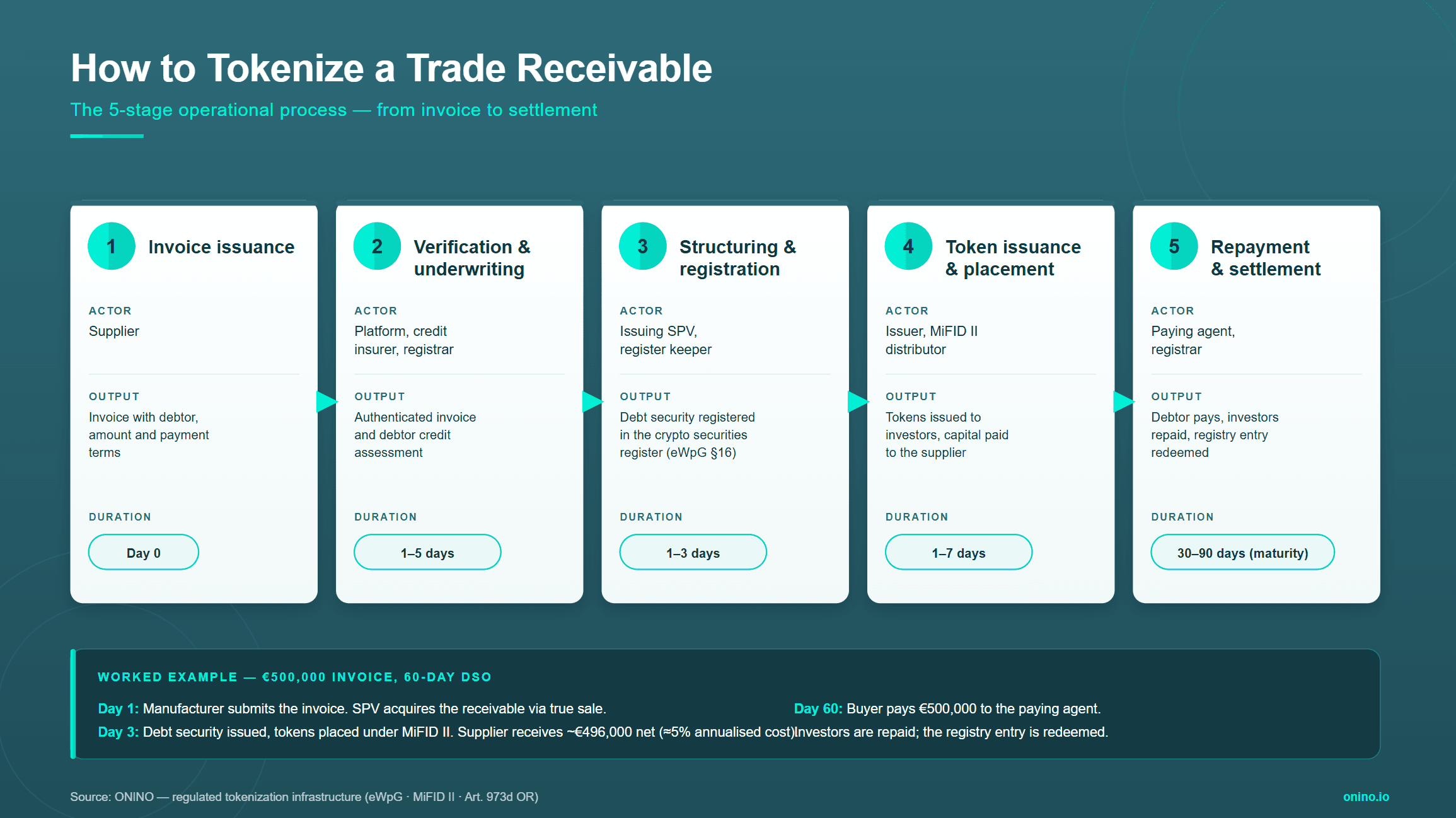

How to tokenize a receivable: the five operational stages

Stage | Actor | Output | Typical duration |

|---|---|---|---|

1. Invoice issuance | Supplier | Invoice with debtor, amount, payment terms | Day 0 |

2. Verification and underwriting | Platform, credit insurer, registrar | Authenticated invoice, debtor credit assessment | 1 to 5 days |

3. Structuring and registration | Issuing SPV, register keeper | debt security registered in crypto securities register | 1 to 3 days |

4. Token issuance and placement | Issuer, MiFID II distributor | Tokens issued to investors, capital paid to supplier | 1 to 7 days |

5. Repayment and settlement | Paying agent, registrar | Debtor pays invoice, investors repaid, registry entry redeemed | Invoice maturity (30 to 90 days) |

Stage 1 starts with a supplier issuing an invoice to a debtor. The invoice must identify the debtor, supplier and the details of the transaction ( amount, currency, due date, payment terms etc). As well as supporting evidence of delivery arrangements, ERP data acceptance records. This matters because the receivable is only financeable if its legally valid.

Stage 2 is where the platform actually verifies invoice authenticity (commonly via ERP integration or copy of the invoice plus debtor confirmation), assesses debtor credit (rating agency data, credit insurance availability), and validates that the receivable is assignable. The legal opinion attaches to the receivable, not the token.

Stage 3 is where the regulated structure is built. A debt security ****is issued by an SPV that has acquired the receivable through true sale. True sale is what enables off-balance-sheet treatment under HGB and IFRS; auditors look at the transfer of risks and rewards, not just legal title, so the SPV must take genuine credit exposure for derecognition to hold. The register keeper

records the instrument under eWpG §16. The instrument may carry credit enhancement, discussed in the next section.

Stage 4 is where the registered instrument is placed with investors. Once the debt security has been created and recorded in the crypto securities register, the issuer or distributor offers the tokens to eligible investors through the agreed distribution channel. Investor onboarding covers KYC, AML, sanctions screening, MiFID II classification, and suitability or appropriateness checks where required. Investors subscribe for the tokens and pay the subscription amount; the proceeds flow through the issuer or SPV structure and are ultimately used to provide financing to the supplier. The token is therefore the transferable digital representation of the registered debt security, while the legal right itself remains anchored in the register and the underlying issuance documents.

Stage 5 closes the cycle. When the debtor pays, the paying agent distributes funds to the registered holders. The registrar marks the entry as redeemed; the on-chain representation is retired accordingly. There is no token burn in the DeFi sense; the legal extinguishment happens in the register.

Worked example

A Bavarian manufacturer holds a €500,000 invoice on a large industrial buyer, payable in 60 days. It needs liquidity now to fund its next production run.

Day 1: The manufacturer submits the invoice to a tokenization platform. The platform verifies the invoice against ERP records and confirms the named obligor. An SPV acquires the receivable via true sale at a discount reflecting the 60 day duration plus credit margin.

Day 3: The SPV issues a debt security registered as a crypto security. The platform distributes the token to investors under MiFID II rules. The manufacturer receives approximately €496,000 in net proceeds, an effective discount of around 0.8% on the invoice value, which annualizes to roughly 5% all-in cost on the 60-day exposure.

Day 60: The buyer pays €500,000 to the paying agent on the original invoice schedule. The paying agent distributes proceeds to the registered holders. The register keeper marks the entry as redeemed. The investors realize the spread net of platform and registry fees.

The economics sit between traditional factoring (typically 1.5 to 5% of invoice value plus fees, single counterparty) and corporate bond issuance (lower spread but minimum tickets and underwriting that exclude most SMEs).

Where tokenized receivables are used

Tokenized receivables are most common in trade finance and supply chain financing, where payment cycles are longer than production cycles. The Asian Development Bank (ADB Trade Finance Gaps Report 2023) estimates the global trade finance gap at $2.5 trillion, with SMEs disproportionately affected.

The second use case is asset-manager portfolio construction. A multi-family office or private credit fund that wants short-duration, asset-backed exposure can build a tokenized receivable sleeve by allocating across multiple verified invoices, with concentration limits per debtor and per sector. Reporting flows through the registry; settlement is automated.

A third use case is treasury-driven self-financing. Corporates with large receivable books can issue tokenized receivables to their own pension fund, sister entity, or external allocators while retaining commercial control of the customer relationship. Unlike factoring, the buyer typically does not need to be notified of the assignment under §354a HGB.

Tokenization vs factoring vs invoice discounting

Feature | Tokenized receivables | Invoice factoring | Invoice discounting |

|---|---|---|---|

Ownership | Investors hold security tokens | Factor owns the invoice | Lender holds a charge |

Investor base | Multiple regulated investors | Single factor | Single bank or lender |

Settlement | On-chain transfer, register redemption | Bank settlement | Internal lender system |

Transparency | Per-invoice, on-chain | Bilateral contract | Bilateral contract |

Disclosure to debtor | Optional under §354a HGB | Usually notified | Confidential |

Typical cost | 3 to 6% effective on 60-day exposure | 1.5 to 5% of invoice value plus fees | EURIBOR plus margin |

Off-balance-sheet | Yes, where true sale | Yes, where non-recourse | No |

Recourse matters and is often the deciding factor. Tokenized receivables are typically non-recourse from the seller's perspective once true sale is documented, with credit risk borne by the investor (or transferred to a credit insurer where insured). Non-recourse factoring offers the same outcome but with a single counterparty and higher pricing for the protection. Recourse factoring is cheaper but keeps the loss on the seller's balance sheet.

The choice is not always exclusive. A treasurer might keep a bank discounting line for routine working capital and use a tokenization programme for the receivables that fall outside the bank's appetite (longer DSO, smaller buyers, cross-border).

Regulatory classification across jurisdictions

Jurisdiction | Typical wrapper | Statute | Regulator |

|---|---|---|---|

Germany | debt security registered as a crypto security | eWpG §16, KWG | BaFin |

Switzerland | Register-uncertificated security | Art. 973d OR, FinfraG, DLT Act | FINMA |

Luxembourg | Securitisation vehicle issuing notes | Securitisation Law 2004, as amended | CSSF |

EU cross-border distribution | Prospectus or ECSPR exemption (€5M / 12 months) | Prospectus Regulation, ECSPR | ESMA, national NCAs |

A tokenized receivable structured as a debt security is a MiFID II financial instrument. It is therefore explicitly excluded from MiCA, which only covers crypto-assets that are not already financial instruments under MiFID II (MiCAR Recital 14, Title III/IV scope). This is the most-misunderstood point in the category. ONINO operates the regulated rails on the MiFID II side, not the MiCA side.

The eWpG entered into force on 10 June 2021. MiCA Titles III and IV apply from 30 December 2024, but the regime does not capture instruments structured as debt security.

Operational risk and credit structure

Tokenizing a receivable does not eliminate underlying credit risk; it relocates it. If the debtor pays late or defaults, the investor bears the loss unless credit enhancement is in place. Three structures are common in practice.

The most-used is a credit insurance wrapper. Insurers such as Allianz Trade, Atradius, or Coface insure the receivable, and the investor inherits the cover. This is standard for investment-grade obligors and pushes effective loss rates well below 1% on insured portfolios (FCI Annual Review 2024).

A second option is a first-loss tranche. The issuer retains a slice of the exposure; investors hold the senior tranche. This aligns incentives and is common where insurance is unavailable or expensive.

The third is over-collateralization through pooling. A pool of receivables backs the tokens; the cushion absorbs first losses. This is typical for SME receivables where individual underwriting is impractical.

Whichever structure applies, the servicer (collection, dispute handling, follow-up) is named in the SPV documentation. Investors should always check who services the receivable on default, not just who originated it.

Costs and eligibility

Tokenized receivable programmes are typically viable from a receivables book of around €2 million upwards, with single-invoice tickets from around €50,000. Below that threshold, the legal and registry fixed costs dominate. Programmes scale efficiently above €10 million in annual issuance.

The cost stack includes the credit spread to investors (the largest component, usually 2 to 5% annualized), platform fees, registrar fees, paying-agent fees, credit insurance premium where applicable, and legal opinion costs amortized across the programme. For most issuers this lands at 3 to 6% effective cost of capital on a 60-day receivable.

To find out how much this would cost, please schedule a meeting with us and we can provide you with a personalised strategy in under 10 minutes.

Let us help you

For issuers and finance teams. If your treasury sits on 30 to 90 days of trade receivables, the question is not whether to release that capital. It is on what infrastructure. ONINO operates the regulated stack across the EU and Switzerland: SPV structuring, Kryptowertpapierregister, MiFID II distribution, and automated repayment from day one.

See how a receivables programme is structured on ONINO →

For asset managers and investor clubs. Tokenized receivables open a short-duration, asset-backed exposure that has historically sat inside factoring books. Each invoice is a separately verifiable, individually priceable position with automated settlement on payment. ONINO operates the issuing rail; allocations flow into your existing custody and reporting setup.

Explore tokenized receivables for asset managers →

Author: Lukas Wipf, CPO and Co-Founder of ONINO. Lukas leads product at ONINO, building regulated tokenization infrastructure for issuers, asset managers, and banks across the EU and Switzerland. Background in private markets and asset-backed finance. Connect on LinkedIn.

Want to learn more how this can be applied to your business?

Read related Articles

Tokenize invoices & trade receivables to unlock working capital faster. Practical guide for SMEs and lenders - covering legal setup, smart contracts & EU compliance.