News

7 Lessons from the US Oil Reserve Tokenization Case Study

From USOR to reserve-backed security tokens: 7 findings from the US market that show asset managers where oil tokenization works, where it fails, and why Europe is ahead

Kristina Stark

Junior Growth Manager

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for regulated tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

The US oil tokenization market is split between speculative meme coins (like USOR, which falsely claimed SPR backing) and credible private-market structures (like LITRO, which requires independent audits and 1:1 reserve-backed token issuance). US regulation is still a grey zone, while Europe's MiFID II framework offers clearer rules for asset managers. Any legitimate oil reserve token needs six things: independent audits, 1:1 issuance, securities classification, enforceable custody, smart contract distributions, and a regulated secondary market. Most products on the market fail that test.

7 Lessons from the US Oil Reserve Tokenization Case Study

Here is a question worth sitting with: what happens when one of the world's most powerful commodities meets one of the most disruptive financial technologies in history?

You get chaos, confusion, a few genuine breakthroughs, and one very loud meme coin called USOR.

The US market has become the world's most visible testing ground for oil reserve tokenization. It has produced credible private-market structures that institutional investors are quietly watching, and it has produced spectacular speculative failures that made headlines for all the wrong reasons. If you are an asset manager trying to figure out what is real here, what is regulatory fiction, and where Europe actually stands, this is the case study you need.

Let's break it down.

Lesson 1: Tokenizing Oil Is Not What Most People Think It Is

Before anything else, let's clear up the single biggest misconception in this space. Tokenizing oil reserves is not the same as trading oil.

I know that sounds obvious. But the confusion is everywhere, and it matters enormously for how you evaluate any product claiming to sit in this category.

When we talk about oil reserve tokenization, we mean representing legal ownership rights to proven crude oil reserves, royalty streams, or specific production rights as programmable digital tokens on a blockchain ledger. Not a futures contract. Not an oil-backed stablecoin. Not a commodity price tracker dressed up in blockchain language. The mechanics, the legal structure, and the risk profile are all materially different from any of those instruments.

Think of it this way: buying a tokenized oil reserve is closer to buying a fractional stake in a producing well than it is to buying a barrel of crude on the open market. The former gives you a legal claim on a specific asset and its revenue. The latter gives you price exposure. These are completely different things, and mixing them up is how asset managers end up in the wrong product for the wrong reason.

Lesson 2: USOR Is the Clearest Warning the Market Has Produced

Let's talk about USOR. Because if you want to understand what oil tokenization is not, this is your case study.

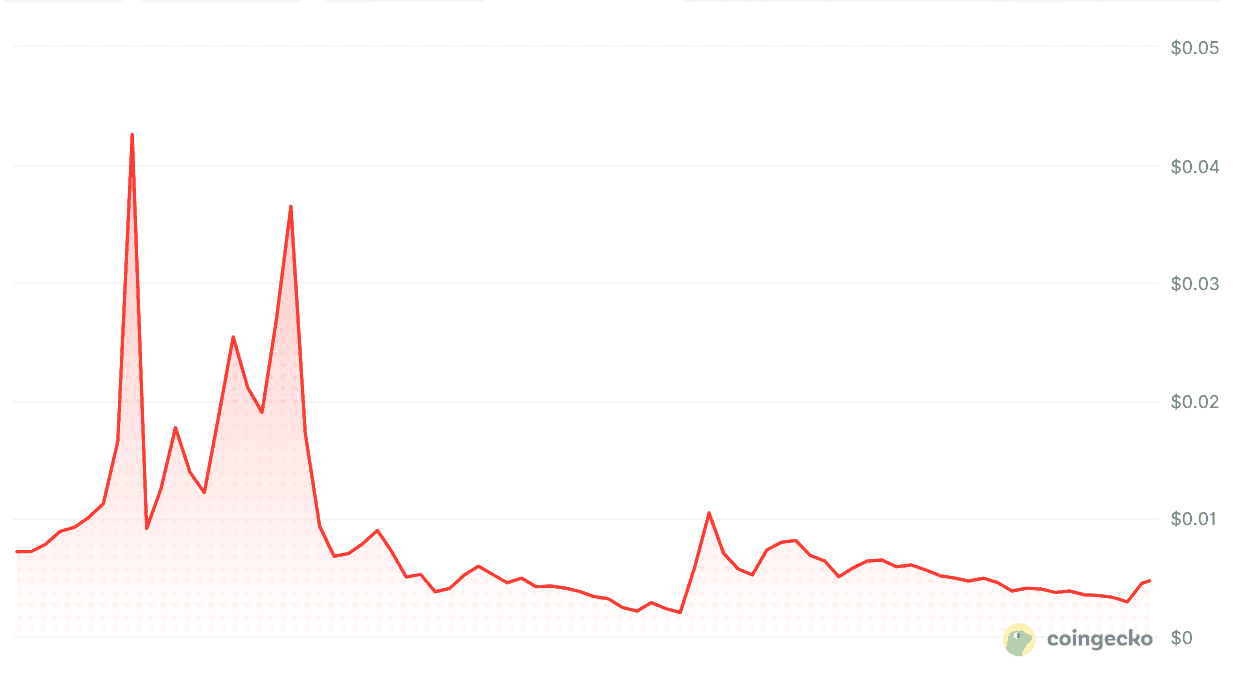

In January 2026, a Solana-based token called USOR exploded across crypto Twitter, TikTok, and Instagram with a compelling claim: it was backed by US strategic oil reserves and poised for a political-style rally tied to Donald Trump. The narrative spread fast. The token peaked at a $55 million market cap and $27 million in 24-hour trading volume within days.

Then analysts started asking questions.

CCN and Yahoo Finance established that tokenizing the US Strategic Petroleum Reserve would require federal legislation, Department of Energy authorization, independent audits, custody agreements, and a regulatory approval framework that simply does not exist at any operational scale. The DOE, which actually manages the SPR, issued no statement. The USOR website contained inaccuracies about US institutions, including references implying the Federal Reserve stores oil. It does not. The Department of Energy does.

A token referencing oil reserves is not the same as a security with a legal claim on those reserves. That gap is where most retail-facing oil token products currently live.

USOR was eventually characterized as a speculative meme coin with no verified reserve backing: heavy on narrative, thin on compliance, and driven by influencer marketing aimed at retail investors who did not check the smart contract before buying in.

The lesson is not that oil tokenization is fraudulent. It's that you need to know exactly which side of that gap any product sits on before you make an allocation decision.

Lesson 3: The Credible US Structures Are Private-Market and Quiet About It

Here is something interesting. Away from the USOR noise, the US market has produced a smaller cohort of structurally sound oil tokenization instruments. You probably have not seen them in your Twitter feed, and that is entirely the point.

These are private-market arrangements where oil and gas operators tokenize working interests, royalty streams, or production rights in specific, producing fields. They are structured as regulated securities under SEC frameworks, they require independently audited reserve verification, and they operate on platforms with defined investor eligibility criteria, typically accredited investors under Reg D exemptions.

The most compelling example to emerge from current market coverage is LITRO, reported by CoinDesk in March 2026. Developed by a former Petronas Trading Corporation business development manager, LITRO mints one token per one verified litre of crude, targeting a January 2027 launch. The INDEX platform behind it requires oil producers to pledge certified reserves, then runs independent audits for quantity, authenticity, and ownership before a single token is minted. "Only audited and verified reserves can be tokenized," the developer explained, with tokens issued on a strict 1:1 basis against confirmed physical volume.

That is the standard. Quiet, rigorous, and the polar opposite of a meme coin launch.

Lesson 4: Fractional Ownership Is the Real Value Proposition for Asset Managers

Let's talk about why this matters for your portfolio construction, specifically.

Oil and gas assets, particularly producing reserves and royalty streams, have historically been inaccessible to institutional investors outside the energy sector. Direct working interest ownership requires operational knowledge, specialist tax structuring, and legal frameworks that price most institutional allocators out before they even start due diligence. Listed energy equities offer exposure, but they carry equity risk, management risk, and give you no direct claim on the underlying reserve value.

Tokenization changes this equation in three specific ways:

Fractional ownership of specific reserve tranches, with entry points on some platforms as low as $50 to $100

Secondary market liquidity for positions that currently have no exit mechanism

Programmable revenue distribution via smart contract, where royalty or production income flows directly to token holders without administrative delay

For asset managers building diversified real asset portfolios, these are not hypothetical benefits. They address a genuine structural inefficiency. The global crude market is approximately $6 trillion. The private reserve base held by independent operators is several times that. The access problem is real, and tokenization is one of the few frameworks that actually solves it at scale.

"Since 2023, retail investor participation in tokenized US shale assets has grown steadily, with over 10,000 individuals joining and user registration rising 30% annually." - GEP Industry Analysis, 2025

Lesson 5: The US Regulatory Framework Has Not Caught Up

This is the most significant structural barrier in the American market, and it is worth understanding clearly because it directly affects how much of this market is actually investable for institutional purposes right now.

Oil reserve tokens in the US currently occupy a regulatory grey zone. The SEC has not issued specific guidance on reserve-backed tokens. The existing commodity and securities framework creates overlapping jurisdictional questions between the SEC, the CFTC, and the Department of Energy that remain unresolved. Operators and platforms are making structuring decisions based on legal opinion rather than settled rule-of-law.

The SEC's Market Structure Subcommittee did vote in March 2026 to recommend the agency move forward on tokenized securities policy, which is a meaningful signal. But a recommendation is not a framework, and a framework is not a regulation.

For institutional asset managers, this creates compliance uncertainty that limits the investable universe to a narrow set of well-documented private placements with robust legal opinions. It is not an impossible market to access. It is just a demanding one with limited standardization.

Lesson 6: Europe Offers a More Defined Legal Path, Even If It Is Demanding

And this is where ONINO's European positioning becomes genuinely relevant to the conversation.

Under MiCA, tokens referencing real assets generally do not fall under the e-money token or asset-referenced token definitions. Oil reserve tokens structured as security tokens, representing a legal claim on a defined underlying asset, fall under MiFID II and the Prospectus Regulation instead. This brings investor protection obligations, disclosure requirements, and secondary market rules that are well-established in European institutional markets.

Here is a side-by-side comparison of the two frameworks:

Dimension | US Framework | EU Framework (MiFID II / MiCA) |

|---|---|---|

Regulatory clarity | Grey zone, evolving | Defined, demanding |

Classification | SEC / CFTC overlap unresolved | Security token under MiFID II |

Investor protections | Varies by structure | Standardised EU obligations |

Prospectus requirement | Reg D / Reg S exemptions typical | Prospectus or qualified investor threshold |

Secondary market | Unregulated or regulated depending on platform | Regulated venue requirement |

Audit requirement | Legal opinion-driven | Enforceable compliance standard |

The EU framework does not make oil tokenization easy. But it makes it definable, and for asset managers who need regulatory clarity as a precondition for allocation, that distinction is everything.

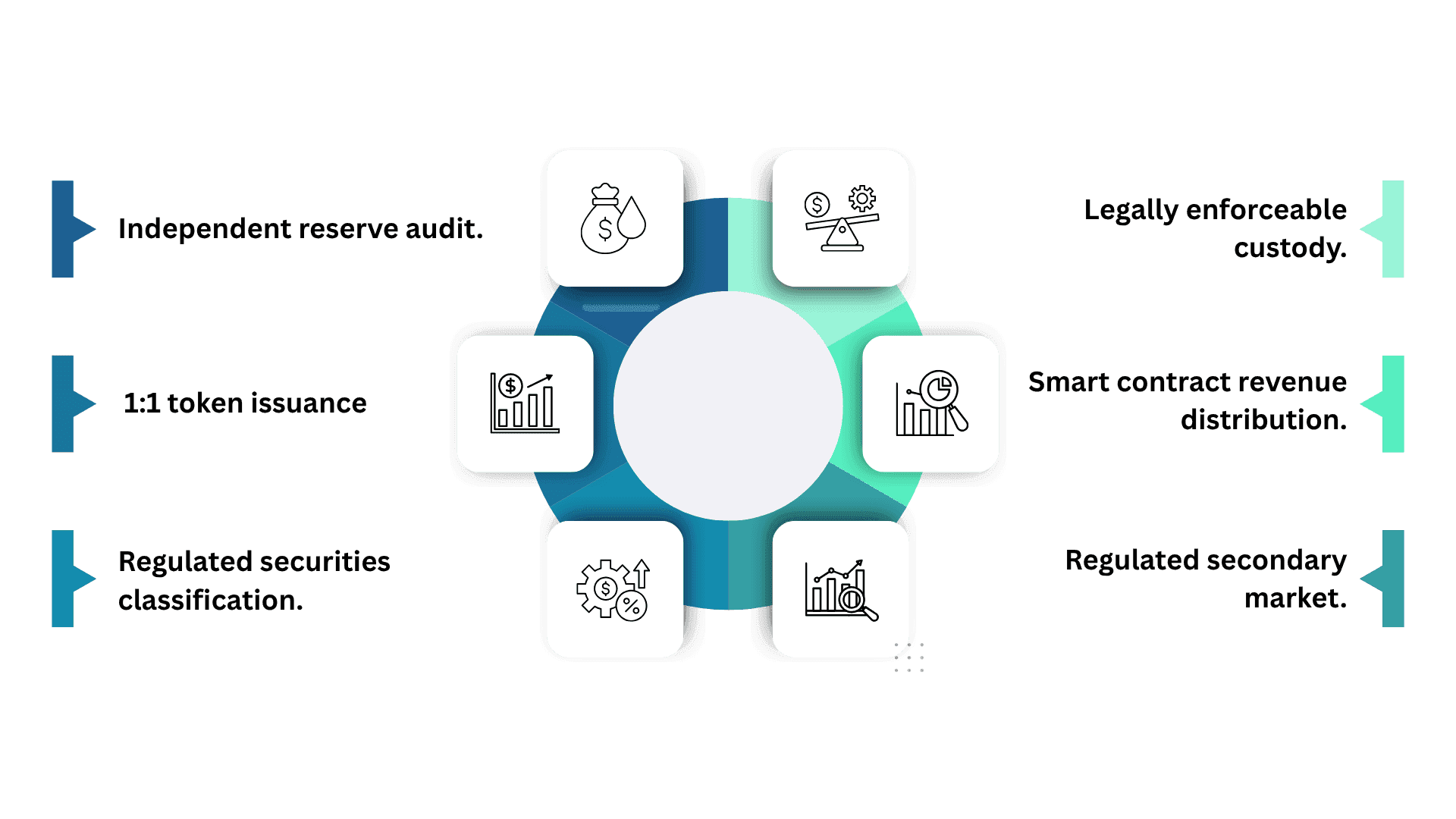

Lesson 7: A Compliant Structure Has Six Requirements That Are Non-Negotiable

Let's end with the practical framework. Based on everything the US market and the emerging European structures have shown us, a structurally sound oil reserve token shares these six characteristics. All six. Not four out of six.

Independent reserve audit. The underlying reserves must be verified by a recognised third party before any token is minted. No audit, no token.

1:1 token issuance. Every token must map directly against a confirmed, audited reserve volume or royalty entitlement. No speculative or unbacked minting.

Regulated securities classification. The issuing entity must operate under a recognised securities framework with appropriate prospectus or exemption documentation.

Legally enforceable custody. The claim on the underlying asset must be legally enforceable, not merely a contractual arrangement that collapses under legal challenge.

Smart contract revenue distribution. Distributions from production output or royalty revenue should flow via smart contract with transparent, on-chain audit trails.

Regulated secondary market. Where secondary market liquidity exists, it must operate through a regulated trading venue, not an unregulated crypto exchange.

These requirements are demanding. They also largely exclude most of what has been marketed to retail investors under the oil tokenization label. For institutional asset managers, that exclusion is a feature, not a limitation. It is how you tell the real from the noise.

ONINO provides regulated tokenization infrastructure for real assets under MiFID II and MiCA. Oil and gas reserves, royalty streams, and energy production rights can be structured as compliant digital securities on the ONINO platform, with full regulatory documentation, investor eligibility controls, and secondary market capability. If you are evaluating oil reserve tokenization as a structured product opportunity, speak to the ONINO team.

FAQ: What Asset Managers Are Actually Asking About Oil Tokenization

Is tokenized oil a good investment?

Structure determines everything here. Speculative tokens claiming oil price exposure or unverified reserve backing carry high risk and limited legal protection. Regulated security tokens backed by audited, producing reserves under a defined legal framework are a distinct instrument category, with risk profiles closer to private credit or royalty financing than to commodity speculation.

When will oil reserves be widely tokenized?

Widespread institutional adoption requires clearer US regulatory guidance, broader standardization of audited reserve verification, and deeper secondary market infrastructure. Compliant private structures are operating now. A truly accessible institutional market is a 3 to 5 year horizon at the earliest.

Who has the largest unproven oil reserves?

Venezuela, Saudi Arabia, and Canada hold the largest proven reserve bases globally. Unproven reserves are, by definition, unaudited and therefore ineligible under any credible compliant tokenization framework. Only independently verified, proven reserves are structurally eligible.

Why does BlackRock want to tokenize assets?

BlackRock has identified liquidity, operational efficiency, and expanded investor access as the primary drivers of its tokenization strategy. Energy and commodity assets are part of a broader real asset allocation thesis in which tokenization reduces structural barriers to entry without altering the underlying risk exposure.

Summary: The 7 Lessons in Brief

The US market has taught us that oil reserve tokenization is not about which meme coin captures the best political narrative. It is about audits, legal structure, regulatory classification, and enforceable custody.

USOR showed us the gap between a compelling story and a compliant instrument. LITRO showed us what the compliant side actually looks like. The EU framework showed us that clear regulation, even demanding regulation, is better than an unresolved grey zone.

If you are an asset manager evaluating this space, the question is not whether oil reserve tokenization is real. It is whether the specific instrument in front of you passes all six requirements above.

Most do not. The ones that do are worth your due diligence.

Want to learn more how this can be applied to your business?

Read related Articles

From USOR to reserve-backed security tokens: 7 findings from the US market that show asset managers where oil tokenization works, where it fails, and why Europe is ahead