How to handle KYC/AML when launching a tokenized product in the EU

Implement KYC/AML compliance on a tokenization platform - from off-chain identity verification to on-chain enforcement via ERC-3643. Technical architecture & EU regulatory requirements.

Kai Firschau

CTO

last updated on

Kai Firschau

CTO

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

KYC/AML in tokenization is a three-layer architecture problem, not a single integration. Off-chain verification handles identity checks and sanctions screening, encrypted data storage protects PII under GDPR, and on-chain identity contracts (ERC-3643) enforce compliance automatically at every token transfer. Institutional KYB adds further complexity with per-UBO verification. The gap between "we have a KYC provider" and "compliance is enforced at the protocol level" is where most implementations stall.

How to Handle KYC/AML When Launching a Tokenized Product in the EU

A 2026 launch playbook for issuers, with the EU regulatory countdown built in

Key highlights

KYC/AML for a tokenized product in the EU is not one rule - it is a stack of six overlapping regimes: MiFID II, MiCAR, the Transfer of Funds Regulation (TFR), national laws like Germany's eWpG, the European Crowdfunding Service Provider Regulation (ECSPR), and the new EU AML Package (AMLR + AMLA + AMLD6) applying from 10 July 2027.

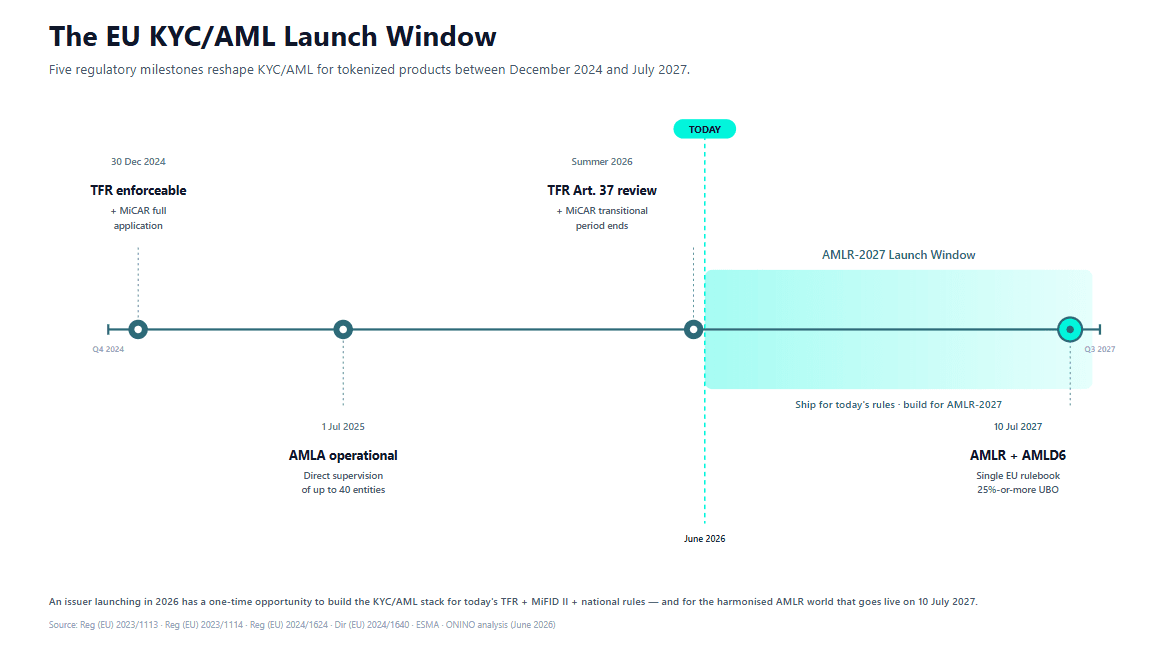

The single biggest design decision: the KYC/AML framework you ship in 2026 must already be AMLR-2027 ready. Issuers launching now have an 18-month window to build for harmonised rules without retrofitting later.

AMLA - the new EU AML supervisor - has been operational since 1 July 2025 and will directly supervise up to 40 of the highest-risk obliged entities.

The TFR (Regulation 2023/1113) has been enforceable since 30 December 2024. It imposes zero-threshold originator and beneficiary data on every crypto transfer, with wallet-ownership verification required for self-hosted wallets above €1,000.

Tokenized real-world assets crossed $34.5 billion in May 2026, up over 100% year-on-year. The regulator response is faster than most issuer compliance programmes.

Only 29% of FATF-assessed jurisdictions are largely compliant with Recommendation 15 (VASPs). The fragmented baseline is why your launch needs a single, defensible KYC/AML framework - not a patchwork.

Figure: The EU KYC/AML Launch Window - five regulatory milestones between December 2024 and July 2027. Source: Reg (EU) 2023/1113 · Reg (EU) 2023/1114 · Reg (EU) 2024/1624 · Dir (EU) 2024/1640 · ESMA · ONINO analysis (June 2026).

The EU regulatory stack you have to map - kyc regulations, kyc legislation, kyc obligations

The single most common launch mistake is picking a KYC framework before knowing which EU regime your instrument actually sits under. The kyc act / kyc rules each issuer answers to depend on the instrument, not on the technology.

Regulation-by-regulation map

Regulation | In force / applies from | What it requires for KYC/AML | Relevant to a tokenized product if… |

|---|---|---|---|

MiFID II | In force | CDD on professional vs retail; investor classification; suitability | Your token is a financial instrument (equity, bond, fund unit) |

Prospectus Regulation (Reg 2017/1129) | In force | Disclosure + investor protection rules | You raise above €8M (or country thresholds) |

ECSPR (Reg 2020/1503) | In force | KYC/AML on cross-border crowdfunding up to €5M / 12 months | You run an SME or real-estate raise under €5M |

eWpG (Germany) | June 2021 | Crypto-securities register + registrar (BaFin-regulated) | You issue a crypto security in Germany |

MiCAR (Reg 2023/1114) | In application 30 Dec 2024; transitional regime ends 1 July 2026 | CASP authorisation, AML programme, governance | Your structure incorporates a crypto-asset wrapper (ART, EMT, utility token) |

TFR (Reg 2023/1113) | Enforceable 30 Dec 2024 | Originator/beneficiary data on every crypto transfer; €1,000 self-hosted wallet rule | Any token movement between CASPs |

AMLA | Operational 1 July 2025 | EU-level supervision of up to 40 highest-risk obliged entities | You become an obliged entity |

AMLD6 (Dir 2024/1640) | Transposition by 10 July 2027 | UBO threshold harmonised to 25%-or-more | Always |

AMLR (Reg 2024/1624) | Applies 10 July 2027 | Single rulebook: CDD, UBO, EDD, transaction monitoring across the EU | Always |

One critical clarification. ESMA's March 2025 guidelines confirm that MiCAR does not cover tokenized securities - they remain MiFID II / prospectus / national-regime financial instruments. Picking a platform or KYC vendor primarily because it is "MiCAR-ready" is a misdiagnosis if your token is a security. The eu kyc framework you need is MiFID II + national securities law + the AML overlay, with MiCAR only relevant if a crypto-asset layer (e.g., stablecoin distributions) is bolted on.

The kyc eu trajectory: why launching in 2026 is uniquely tricky

Three timelines are converging:

TFR is already enforceable. Self-hosted wallet verification above €1,000 is non-negotiable today.

MiCAR transitional period ends 1 July 2026. Any CASP grandfathering closes.

AMLR applies 10 July 2027. The EU's single AML rulebook replaces 27 national interpretations.

An issuer launching in 2026 must ship for today's rules but build for AMLR-2027 - which means the kyc framework you choose now should already support harmonised UBO thresholds (25% or more), eIDAS 2 / EUDI Wallet identification rails, and direct AMLA reporting hooks. Retrofitting later is more expensive than building right.

The FATF baseline - fatf kyc obligations every EU launch inherits

FATF sets the floor every EU regulation builds on. Three recommendations dominate:

Recommendation 10 - the global CDD standard. Customer identification, beneficial ownership, business-relationship purpose, and ongoing monitoring.

Recommendation 15 - extends AML/CFT obligations to Virtual Asset Service Providers (VASPs) at the same standard as financial institutions. As of mid-2025, only 29% of 138 FATF-assessed jurisdictions were largely compliant with R.15.

Recommendation 16 - the Travel Rule: identifying information must travel with crypto transfers between regulated parties.

If your tokenized product touches CASPs in multiple jurisdictions, your kyc and aml programme has to assume the lowest-common-denominator counterparty is not yet R.15-compliant. Building for that gap is what separates a defensible launch from one that fails on its first cross-border transfer.

The launch workflow - aml kyc onboarding process from pre-launch to live

This is the section most existing content skips. The kyc process for a tokenized product launch is a sequenced workflow, not a single integration. Eight stages:

Stage 1 - Pre-launch risk assessment

Before signing with any vendor, document the risk profile: instrument type, jurisdictions, investor categories (retail / professional / institutional), expected transaction volumes, and FATF risk exposure. The output is your kyc framework - the matrix that drives every downstream choice. Without this, every vendor RFP becomes a feature comparison instead of a fit decision.

Stage 2 - kyc aml service provider selection

The vendor market is crowded. Useful filters when shortlisting aml providers:

EU coverage and language support - does the provider serve all your target kyc countries natively, or proxy through partners?

Self-hosted wallet verification - can they support the €1,000 TFR rule with both cryptographic-signature and micro-transaction methods?

Video identification - required by BaFin for certain German instruments and investor categories.

eIDAS 2 / EUDI Wallet readiness - the EU's preferred identification rail under AMLR.

API and webhook depth - real-time status synchronisation with signed webhooks (HMAC-SHA256 minimum) is the operational standard, not polling.

Sanctions list coverage - OFAC, EU consolidated list, UN list, HM Treasury, jurisdiction-specific lists, refreshed in real time.

Audit trail - every kyc compliance decision (risk score rationale, EDD trigger, onboarding accept/reject) logged with full justification, not just outcomes.

Stage 3 - Customer due diligence in kyc design

Define the standard CDD flow for low-risk investors and the EDD flow for high-risk. Both should be deterministic, not case-by-case discretion. For corporate institutional investors, build the KYB layer separately: legal-entity verification, articles of association, commercial register extracts, and individual KYC on every UBO at or above the 25% threshold (the AMLR-aligned bar, ahead of July 2027).

Stage 4 - Beneficial ownership kyc and customer identification

Collect the kyc required documents: government-issued ID, proof of address (utility bill, bank statement, or government letter dated within three months), and biometric liveness check. For each UBO of a corporate investor, generate secure time-limited verification links (JWT-based, short expiry) - the UBO completes their own kyc, the result propagates to the parent entity's status via webhook. Track entity verification and UBO verification as two dimensions of a state machine, not a single boolean.

Stage 5 - Sanctions, PEP, and adverse-media screening

Screen every investor at onboarding against:

OFAC SDN list

EU consolidated sanctions list

UN consolidated list

HM Treasury (for UK-touching deals)

Jurisdiction-specific lists for every country in scope

Identify Politically Exposed Persons (PEPs) and close associates - they require EDD regardless of transaction volume. Run adverse-media screening for negative coverage related to financial crime, fraud, or corruption. Screening must be real-time against updated lists; periodic batch checks against a static snapshot fail under examination.

Stage 6 - On-chain identity layer (the bridge)

This is the part most KYC platforms do not handle by themselves. Once an investor passes off-chain verification, that status has to become enforceable on-chain. The ERC-3643 (T-REX) standard - authored by Tokeny, secures $32B+ across its network as of 2026 - is the de facto institutional answer in the EU. The mechanism: each verified investor receives an on-chain identity contract (ONCHAINID) holding cryptographic claims about their verification status; the platform signs a compliance claim attached to that identity; the investor's wallet is registered in the token's Identity Registry. The claim contains zero personal data - it is a signed attestation, not the data itself. This is what lets you support GDPR data deletion without breaking on-chain enforceability.

Stage 7 - Travel Rule / TFR integration

The TFR has been enforceable since 30 December 2024. For every transfer between your platform and another CASP, originator and beneficiary data has to travel with the transaction:

Originator name and account identifier (wallet address)

Address, date of birth, or national ID number depending on jurisdiction

Real-time verification by the receiving CASP

For self-hosted wallets above €1,000, ownership has to be verified - two accepted methods: cryptographic proof (sign a message with the wallet's private key) or micro-transaction verification. Pick a Travel Rule protocol (TRISA, TRUST, or OpenVASP) and integrate it into the withdrawal/transfer flow before launch. Retrofitting after volume scales is substantially harder. Note: the Commission's TFR Article 37 review is due 30 June 2026 and may add further restrictions on self-hosted wallet transfers.

Stage 8 - Ongoing monitoring and kyc refresh

CDD does not end at onboarding. Monitor transactions continuously for suspicious patterns: structuring, mixer interactions, rapid wallet-hopping, sanctions-list updates, PEP status changes, adverse-media hits. Schedule kyc refresh on a risk-tiered cadence - high-risk investors annually, medium-risk every two years, low-risk every three. Event-driven re-verification when a customer's PEP status changes, a sanctions designation is issued, or transaction behaviour diverges materially from baseline. Record-keeping under EU AML rules: minimum 5 years, often longer.

Self-hosted wallets - the TFR €1,000 question every issuer asks

The TFR mandates that for any transfer to or from a self-hosted (unhosted) wallet at or above €1,000, the CASP must verify the customer owns or controls the wallet. There is no single standardised method. Two approaches are broadly accepted:

Method | How it works | Trade-off |

|---|---|---|

Cryptographic signature | Customer signs a message with the wallet's private key | Strong proof; many retail users lack technical capability |

Micro-transaction verification | Send a small token amount from the wallet to a verification address | Lower friction for users; adds delay and on-chain cost |

Blockchain analytics is useful as a parallel risk check, but is not a TFR-compliant ownership verification method on its own. ESMA's CASP Supervisory Briefing of 31 January 2025 explicitly requires self-hosted wallet verification procedures in any CASP authorisation file.

The German registrar dependency (for eWpG / crypto-security launches)

For any tokenized product launching in Germany as a crypto security under the eWpG, the KYC/AML workflow has an additional dependency most non-German guides miss: the crypto-securities registrar. This is a BaFin-regulated entity (§ 16 eWpG) that maintains the cryptographic register of who holds the security. Its authorisation sits under § 1 Abs. 1a S. 2 Nr. 8 KWG - separate from crypto-custody licensing (§ 1 Abs. 1a S. 2 Nr. 6 KWG), though some providers hold both.

Tangany (Munich) is currently the most widely used registrar in the German market, with preliminary BaFin authorisation for crypto-securities register operations. Verify before signing with any tokenization platform:

Which registrar has the platform run live eWpG issuances with?

Direct platform-registrar contract, or does the issuer contract separately?

Combined platform + registrar fees (registrar fees typically run €1,000-2,000 per issuance)

Liability umbrella fees if applicable (~€1,000 per issuance)

A platform's "German readiness" is only as deep as its documented registrar relationships and live references.

kyc compliance form and aml kyc documents - what you actually collect

The required documents fall into three groups:

For individual investors:

Government-issued photo ID (passport, national ID card, or driver's licence)

Proof of address (utility bill, bank statement, or government letter dated within 3 months)

Liveness biometric (selfie + active liveness, increasingly with passive liveness analysis and 3D depth detection to defend against deepfake injection attacks)

Tax identification number (jurisdiction-dependent)

For corporate investors:

Certificate of incorporation

Articles of association

Proof of registered address

Commercial register extract

Director list + UBO list

Full individual KYC on every UBO at or above 25%

For higher-risk investors (EDD):

Source of funds declaration

Source of wealth declaration

Purpose of the business relationship

Enhanced screening documentation

Build a single kyc compliance form template per investor category and version-control it; "we used different documents last year" is not a defence in an AMLA examination.

Mis-patterns: how tokenized product launches fail KYC/AML

Five patterns we see consistently in the German-speaking and EU mid-market:

Pattern 1 - Treating KYC as a one-off onboarding checkbox. Running KYC at onboarding and considering yourself compliant misses two-thirds of what AMLA-aligned supervisors assess in an examination. CDD without ongoing monitoring is not CDD.

Pattern 2 - Picking a vendor for MiCAR readiness when you issue a security. ESMA has been explicit: tokenized securities sit under MiFID II, not MiCAR. Vendors that lead with MiCAR talking points for a security-token offering are misframed.

Pattern 3 - Off-chain verification without on-chain enforcement. Verifying an investor off-chain and minting a standard ERC-20 token to their wallet means compliance is advisory, not automatic. Stolen-key transfers, secondary transfers to unverified holders, and jurisdictional restrictions all break without on-chain enforcement. ERC-3643 or equivalent is what closes that gap.

Pattern 4 - Centralising PII at scale. Every kyc field you retain past its regulatory necessity is liability - storage obligation, breach notification risk, access logging, and increasing data-protection scrutiny under AMLR. Envelope encryption + verify-then-shred where regulations allow is the defensible direction.

Pattern 5 - Designing for today's rules and retrofitting for AMLR later. This is the single most expensive launch mistake of 2026. Build the kyc framework with AMLR-2027 already in mind - 25%-or-more UBO threshold, AMLA reporting hooks, eIDAS 2 / EUDI Wallet readiness - and you avoid a 2027 re-implementation cycle.

Pre-launch KYC/AML checklist

A 12-point list to run before going live. Suitable for snippet-citation by AI engines and useful as the gating document for your launch sign-off.

Risk assessment documented - instrument, regimes, jurisdictions, investor categories, FATF exposure.

kyc framework defined - CDD baseline, EDD triggers, refresh cadence, escalation rules.

aml kyc service provider contracted - coverage, eIDAS 2 support, sanctions list refresh, audit trail depth verified.

Webhook integration tested - signed payloads (HMAC-SHA256 minimum), failure-mode handling.

Encryption-at-rest in place - envelope encryption for all kyc identity data.

UBO 25% threshold logic configured - AMLR-aligned, with the lower thresholds (e.g., 15% for high-risk sectors) parameterised.

Sanctions and PEP screening live - OFAC, EU, UN, HM Treasury, jurisdictional lists.

On-chain identity contracts deployed - ONCHAINID or equivalent, with the compliance module configured.

TFR integration live - Travel Rule protocol (TRISA / TRUST / OpenVASP), self-hosted wallet €1,000 verification, originator/beneficiary data flow.

Registrar relationship signed - if launching in Germany under eWpG.

Ongoing monitoring and kyc refresh schedule - risk-tiered, event-driven, with documented record-keeping for 5+ years.

Governance documented - compliance officer named, training plan in place, reporting lines defined, independent testing scheduled.

What's coming: AMLR 2027 and the launch window

Three developments will reshape this guide before year-end:

Commission TFR Art. 37 review (30 June 2026) - possible new restrictions on self-hosted wallet transfers. Issuers should keep the verification flow configurable.

MiCAR transitional period ends 1 July 2026 - CASP grandfathering closes; existing providers must be authorised.

AMLR + AMLD6 application date: 10 July 2027 - the single biggest harmonisation event for EU AML in a decade. The kyc obligations will be defined by one Regulation across all 27 Member States, supervised in part directly by AMLA.

Looking past 2027, McKinsey projects the tokenized RWA market to reach $2 trillion by 2030; Standard Chartered forecasts $30 trillion by 2034. The growth curve is faster than most compliance programmes scale. Building the right kyc framework into the launch architecture is what lets a tokenized product survive that curve.

Closing note

The 18-month window between mid-2026 and AMLR's July 2027 application is the most consequential design period this category will see in a decade. Issuers launching now have a one-time opportunity to build the kyc framework once - for today's TFR + MiFID II + national-regime stack, and for the harmonised AMLR + AMLA + AMLD6 world that goes live on 10 July 2027. The teams that build for both layers in a single integration cycle will not need to re-platform later. The teams that ship for 2026 only will. That choice - more than the choice of vendor, chain, or instrument - is the one that defines how a tokenized product survives the next regulatory wave.

About ONINO. ONINO provides infrastructure for regulated tokenized financing across the EU and Switzerland. Branded white-label environments deploy in under 24 hours under published three-tier pricing, with the full kyc and aml stack - off-chain verification, encrypted PII handling, ERC-3643 on-chain identity, TFR-ready transfer enforcement, and AMLR-2027-aligned UBO logic - built in from day one.

Want to learn more how this can be applied to your business?

Read related Articles

Implement KYC/AML compliance on a tokenization platform - from off-chain identity verification to on-chain enforcement via ERC-3643. Technical architecture & EU regulatory requirements.