Tokenized Fund Lifecycle Management: From Subscription to Redemption

How tokenized fund lifecycle management works in practice: subscriptions, NAV, distributions, LP reporting, and redemptions for MFOs and SPV operators.

Kristina Stark

Junior Growth Manager

last updated on

Kristina Stark

Junior Growth Manager

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Tokenized fund vehicles do not just lower the cost of issuance. They restructure the entire operational lifecycle into a single, queryable, audit-ready system. Subscriptions become whitelist transactions. NAV updates become signed oracle events. Distributions become smart-contract payouts. LP reporting becomes a permissioned data feed instead of a quarterly PDF. The result is the same fiduciary work done with around 70% less manual ops time, and an audit trail that holds up under regulator review.

Tokenized Fund Lifecycle Management: Cap Table, NAV, and LP Reporting on One Regulated Stack

For multi-family offices, wealth managers, and SPV operators running regulated vehicles in Europe, the operational question is rarely "should we tokenize?" anymore. It is "how do we run the full fund operating model on this infrastructure?" Tokenized fund lifecycle management is the practical answer. It covers every step that happens after the offering closes: investor subscriptions, the cap table, NAV calculation, distributions, LP reporting, and redemptions, all unified on a regulated digital securities stack. For operators evaluating modern cap table management software or an alternative investment fund administrator stack, this is the operating model that ties those tools together.

This guide walks through each phase of that lifecycle as it actually runs in production today under the EU regulatory perimeter (eWpG, MiFID II, AIFMD where applicable), and then shows how the layers fit together on ONINO.

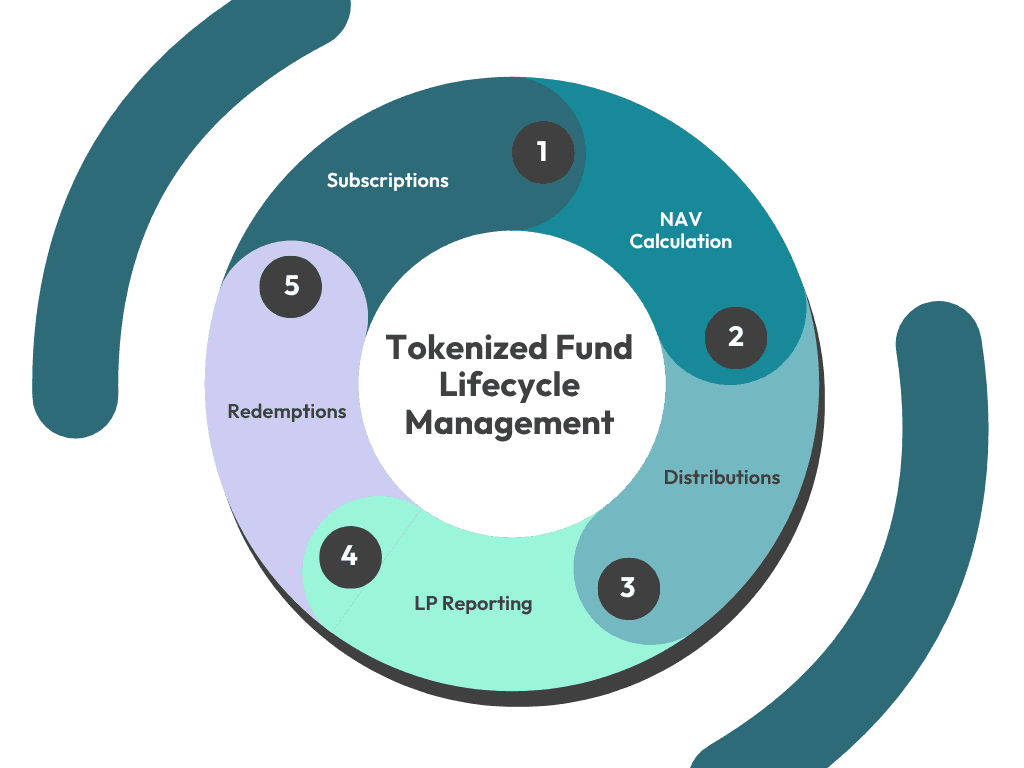

1. Subscriptions and the Cap Table: From PDF to Whitelisted Wallet

A traditional fund subscription is a PDF, a wet signature, a wire confirmation, an entry in a transfer agent's register, and three to five emails confirming each step. Tokenized fund subscription replaces that workflow with one continuous flow:

Investor onboarding and KYC/AML. The investor completes identity verification under AMLD6 standards, accreditation classification (qualified investor under AIFMD or MiFID II professional client), and tax residency declarations. Most ONINO deployments run this through a Cashlink-integrated identity layer for BaFin-compliant onboarding.

Wallet whitelisting. Once approved, the investor's wallet receives an ONCHAINID identity contract on the ONINO platform tied to their verified attributes. That identity is now eligible to receive transfers of the fund token.

Capital call execution. The LP signs the subscription agreement digitally, transfers the subscription amount to the fund's collection account, and receives the corresponding ERC-3643 fund tokens minted to their whitelisted wallet.

Cap table update. The cap table is the token contract itself. There is no parallel spreadsheet. There is no quarterly transfer agent reconciliation. The chain is the source of truth. This is where modern cap table management software for fund vehicles differs from startup-equity tools: the register enforces qualified-investor rules on every transfer, attests holdings cryptographically, and removes the transfer-agent layer that traditional capitalization table management software still depends on. Cap table management platforms built for funds expose the same data to the GP, the depositary, and (with permissioned access) the LP, without the quarterly sync.

For SPV operators running club deals or feeder vehicles into private market opportunities, this collapses what used to be a 15-step process into roughly four steps that can be completed in a single business day.

What this does not solve

Investor diligence is still an offline process. Subscription agreements still require legal review. AIFMD-licensed managers still file the same regulatory notifications they always file. Tokenization removes operational friction from the back office, not the front office.

2. NAV Calculation: From Quarterly PDF to On-Chain Oracle

NAV is the heartbeat of fund lifecycle management. In a traditional fund, NAV is calculated by the fund administrator (typically a third party such as Citco, IQ EQ, or Apex) at a defined cadence (monthly for most private funds, quarterly for less liquid strategies, daily for liquid alternatives), then published to LPs as a PDF or via a portal.

In a tokenized fund, NAV becomes structured data. Three patterns are common in production today:

Off-chain calculation, on-chain publication. The fund administrator still computes NAV using their existing models (DCF for illiquid assets, mark-to-market for traded positions, hybrid models for mixed portfolios). Instead of publishing a PDF, the administrator (or an authorized signer) writes the new NAV per token to a price oracle contract. LPs and downstream systems can now query that oracle programmatically.

Hybrid valuation. For funds holding a mix of illiquid and on-chain assets, on-chain components can be valued in real time while illiquid components are updated at the administrator's calculation cadence. The combined NAV is published on a defined schedule (commonly monthly or quarterly).

Independent NAV verification. A second party (the depositary under AIFMD, or an audit firm) signs an attestation that the published NAV matches the underlying calculation. The signed attestation lives on-chain and is queryable by any LP or regulator.

The underlying valuation methodology does not change. The publication, accessibility, and verifiability of the NAV does.

3. Distributions: Smart-Contract Payouts That Reconcile Themselves

Once NAV is established and a distribution is approved by the GP or fund manager, the actual payment to LPs is where tokenized funds achieve their largest operational savings.

In a traditional fund, the distribution path runs through five steps: fund admin computes per-LP entitlement, the bank initiates ACH or SEPA transfers, LPs reconcile receipts against expected amounts, tax statements (K-1, KESt) are issued at year end, and the fund admin files final distribution reports.

In a tokenized fund operated on a regulated white-label stack, the same distribution runs as four steps: the distribution smart contract is loaded with the per-token entitlement, LPs claim (or auto-receive, depending on configuration) their pro-rata payment in EUR stablecoin or via an integrated SEPA payout rail, the distribution event is logged on-chain with the per-LP amount, timestamp, and tax category, and year-end tax reporting pulls from the same on-chain record.

The reconciliation step disappears because there is nothing to reconcile. The chain holds the only authoritative record of who received what and when. For German funds, KESt withholding can be configured at the smart-contract level for resident LPs, with non-resident handling routed through the existing custodian relationship.

4. LP Reporting: A Permissioned Data Feed, Not a Quarterly PDF

This is the area where tokenized fund lifecycle management most visibly improves the LP experience.

A standard private fund LP receives a quarterly capital account statement (PDF), an annual audited financial statement (PDF), a K-1 or local tax equivalent once a year (PDF), and ad-hoc notices about valuation events, capital calls, and distributions (email). LPs spend the rest of the time guessing about their position.

On a tokenized fund stack, the same LP gets:

A real-time wallet position showing token balance, current NAV, and accumulated distributions

Permissioned access to underlying holdings data (where allowed under the LPA)

An automated capital account roll-forward updated after every NAV publication

One-click export to any major reporting standard (ILPA quarterly template, Solvency II look-through, MiFID II costs and charges)

Real-time access to the audit trail for any reportable event

For MFOs and wealth managers handling 20 to 100 client portfolios across 5 to 30 underlying funds, the consolidation work that previously consumed an analyst-week per quarter compresses into an automated dashboard refresh. The LP-facing portal sits on top of the same on-chain data feed, branded under the MFO's name where the white-label model is used.

5. Redemptions: Programmable Liquidity Within Closed-End Constraints

Redemption mechanics in tokenized funds are constrained by the same regulatory and structural realities as traditional funds. A closed-end private equity fund does not become open-ended just because the LP interest is tokenized. What changes is the precision with which the redemption rules that already exist can be implemented.

Three redemption patterns are common:

Open-ended liquid funds. Daily or weekly redemption windows are coded into the smart contract. LPs submit redemption requests to a queue, the GP approves or pro-rates based on available liquidity, and the redemption is settled in EUR (or the relevant fund currency) within the LPA-defined settlement period. Gates, side pockets, and lock-up rules are enforced programmatically.

Closed-end funds with distribution waterfall. The fund holds tokens until the underlying assets are realized. The smart contract handles the waterfall: return of capital first, then preferred return, then GP catch-up, then carried interest. Each LP receives their pro-rata share at each waterfall trigger.

Secondary market exit. For LPs who need liquidity before the fund's natural redemption events, a regulated private markets venue can match buyers to sellers, with all transfer-eligibility rules (qualified investor checks, jurisdictional restrictions, lock-up status) enforced at the protocol level. The fund manager retains visibility and approval rights consistent with the LPA.

The honest version of this section: secondary liquidity for tokenized private fund interests in Europe is real but still thin in 2026. Order books exist, deals do clear, and pricing is improving as more issuers populate the supply side. It is not yet a deep liquid market for every fund vintage and every strategy. Structuring decisions should assume current market depth, not a future state.

Choosing an Alternative Investment Fund Administrator Stack

For managers evaluating Citco, IQ EQ, Apex, or Gen II, the question is not whether the traditional fund administrator delivers the work. They do. The question is what an alternative fund administrator stack looks like once registry, cap table, distributions, and LP reporting all run as software.

A modern fund administrator stack collapses three legacy roles into one data layer. The transfer agent alternative is the smart-contract register, which holds the cap table and enforces transfer rules at the protocol level. The investor reporting layer reads the same register, so capital account roll-forwards, ILPA quarterly templates, and Solvency II look-through data fall out of the same source. Depositary attestation under AIFMD is preserved, a fund administrator alternative is not a replacement for the depositary, it is a replacement for the manual reconciliation, the PDF distribution, and the quarterly cap table sync.

What the modern fund administrator model does not change: AIFMD-licensed managers still file the same regulatory notifications, AIFMs still report to BaFin or the relevant NCA on the same cadence, the depositary still attests valuations and safekeeps assets, and the legal structure of the fund is unchanged. What changes is the operating cost and the audit-trail quality of the fiduciary work itself.

For an MFO running 20 to 100 client portfolios, the typical operational outcome of moving to an alternative investment fund administrator stack is a 60-75% reduction in analyst-hours spent on reconciliation, an end to quarterly capital account back-and-forth, and a real-time investor portal replacing the email-and-PDF distribution model.

How ONINO Unifies Tokenized Fund Lifecycle Management

The five operational stages above can be implemented on different stacks. They do not have to be unified. But running them on disconnected systems re-creates the manual reconciliation work that tokenization was supposed to remove.

ONINO unifies the lifecycle in the following way:

Lifecycle stage | Traditional stack | ONINO unified stack |

|---|---|---|

Subscription | Subscription docs, wire, transfer agent | ONCHAINID identity, ERC-3643 mint, Cashlink registry |

NAV calculation | Fund admin PDF | Oracle contract signed by fund admin or depositary |

Distributions | Bank transfers, manual reconciliation | Distribution smart contract, EUR rail integration |

LP reporting | Quarterly PDF | Real-time portal, ILPA-format export |

Redemptions | Manual queue, transfer agent | Programmable redemption, regulated secondary venue |

The compliance perimeter sits at the platform layer. eWpG registry duties are handled by Cashlink as the BaFin-supervised crypto-securities registrar. KYC and AML run under AMLD6 standards through integrated providers. AIFMD obligations remain with the fund manager, but reporting and depositary integration are streamlined through the same data layer.

For SPV operators, the operational result is the ability to spin up a new vehicle in roughly 24 hours and run its full lifecycle without building tech. The Volksbank partnership, 8+ live platforms, and €35M of tokenized capital handled to date are the institutional proof points behind that claim.

The white-label option lets you operate this entire stack under your own brand. ONINO holds the regulatory infrastructure; you keep the client relationship, the LP portal, and the deal economics. For wealth managers building toward a unified view of private markets exposure, this is the architecture that makes that view possible.

Book a Demo

If you are evaluating tokenized fund lifecycle management for an existing or planned vehicle, the next step is a working session. Walk through your fund's specific lifecycle requirements (subscription cadence, NAV approach, distribution waterfall, LP reporting standard, redemption mechanics) against ONINO's reference architecture. Most calls take 45 minutes and produce a concrete fit assessment, including which regulatory framework (eWpG, AIFMD, ECSPR) best maps to your vehicle.

Want to learn more how this can be applied to your business?

Read related Articles

How tokenized fund lifecycle management works in practice: subscriptions, NAV, distributions, LP reporting, and redemptions for MFOs and SPV operators.