Business

Where does tokenized debt actually unlock liquidity for bonds and loans?

Tokenized debt explained: how bonds, subordinated loans, and convertibles get issued under the EU DLT Pilot Regime, plus where liquidity actually comes from.

Lukas Wipf

CPO & Co-Founder

last updated on

Lukas Wipf

CPO & Co-Founder

Share

Contact Us

ONINO provides infrastructure for digital & tokenized financing across the EU and Switzerland.

On this page

Quick Takeaway

Tokenized debt is not a crypto product, and it does not change what a bond or a loan is in legal terms. It changes how the instrument is issued, registered, serviced, and transferred. Under the EU DLT Pilot Regime, MiFID II, and the EU Prospectus Regulation, issuers can structure conventional bonds, subordinated loans, profit participation rights, and convertible notes through regulated digital infrastructure, with the investor register, payment schedule, and transfer logic running on a platform rather than across a chain of intermediaries. Liquidity follows when the post-trade plumbing stops being the bottleneck.

Tokenized Debt in Europe: How Bond Tokenization Unlocks Liquidity Under the EU DLT Pilot Regime

What does it mean for a bond or a loan to be tokenized?

A tokenized debt instrument is a conventional debt contract - bond, subordinated loan, profit participation right, or convertible note - issued and managed through a regulated digital platform rather than through paper certificates and intermediary chains. The legal character is unchanged: the investor remains a creditor with a claim to interest and principal, and ordinary securities law continues to apply. What changes is the record and the rails.

Investor entries sit in a digital register, subscriptions and transfers are executed through the platform, and corporate actions such as coupon payments are administered programmatically. The output looks the same to the investor and to the regulator. The cost of producing it is roughly an order of magnitude lower.

Bond tokenization is an operations story, not a technology story. Most market commentary frames it as a blockchain question. In practice, every issuer we talk to ends up asking the same operational questions: who maintains the register, how do coupons get paid, how does the investor exit, who is liable when something breaks. The token is the smallest part of the answer.

What stays the same vs. what actually changes

Stays the same | Changes |

|---|---|

Investor's legal claim to interest and principal | Medium of the register (paper/CSD becomes DLT or e-securities entry) |

Prospectus obligation thresholds | How the prospectus, KID, and offering memorandum are distributed |

MiFID II suitability and appropriateness | How those checks are evidenced (per-investor digital audit trail) |

Tax treatment of coupon income | How withholding is calculated and applied |

Insolvency ranking of the instrument | How collateral and ranking are reflected in transfer logic |

KYC and AML obligations | Where the data lives - one-time onboarding, reused across offerings |

The first column is why your lawyers will tell you tokenization does not fundamentally change anything. The second column is why your operations team will tell you it changes everything.

Which debt instruments are practical candidates for digital issuance?

Four instrument families cover the majority of European tokenized-debt activity in 2026. Plain-vanilla bonds and notes work well because the cash-flow logic is simple and the standardisation translates cleanly into a smart contract. Subordinated loans, widely used in real estate and SME growth financing, benefit from the standardised distribution that a platform provides; in legacy form they require bilateral negotiation per investor. Profit participation rights, which sit between debt and equity, are the most operationally expensive instrument to administer manually, so the gain from automating profit-distribution calculations and payouts is largest there. Convertible notes encode the conversion trigger as a smart-contract condition, which gives every party an auditable record of when and how the debt becomes equity.

Instrument | Economic profile | Where digital issuance helps most |

|---|---|---|

Senior or unsecured bond | Fixed coupon, fixed maturity | Faster issuance, lower distribution cost, programmable coupons |

Subordinated loan | Higher yield, ranks behind senior creditors | Multi-investor distribution at fundraise scale |

Profit participation right | Variable return linked to performance | Automated distribution against audited results |

Convertible note | Debt that converts to equity on trigger | Programmatic conversion, on-chain cap table record |

Where does the EU DLT Pilot Regime fit in?

Regulation (EU) 2022/858, the DLT Pilot Regime, applies from 23 March 2023 and lets authorised firms operate three new market infrastructure types under targeted exemptions from MiFID II and CSDR: a DLT multilateral trading facility, a DLT settlement system, and a combined DLT trading and settlement system. The framework is calibrated to bonds, other forms of securitised debt, and money-market instruments where each issuance is below €1 billion; the aggregate market value of all instruments on a venue is capped at €6 billion, with a transition obligation triggered at €9 billion. The Pilot is set to run for at least three years and is supervised by national competent authorities with ESMA in a coordination role.

The Pilot Regime is not the only path. Most practical tokenized debt issuances in Europe still run through national electronic-securities frameworks rather than DLT trading venues, because the issuance volume sits below the threshold where a regulated trading venue is needed. The DLT Pilot becomes relevant when the issuer wants secondary-market trading on a DLT infrastructure under a single regulatory permission.

The practical rule of thumb: treat the DLT Pilot Regime as a secondary-market tool, not an issuance tool. Issue under national e-securities law; opt into the DLT Pilot when you need a regulated trading venue.

Which European jurisdiction should you issue tokenized debt under?

Four national frameworks dominate tokenized debt issuance in the EU and Switzerland in 2026. Each has a different fit depending on the instrument and the investor base.

Jurisdiction | Framework | Best fit for |

|---|---|---|

Germany | eWpG (Electronic Securities Act, 2021) | Bearer bonds, fund units; central or crypto-securities register |

France | Blockchain Order 2017 + 2018 decree | Unlisted equity and debt securities via DEEP (Dispositif d'Enregistrement Electronique Partage) |

Luxembourg | Blockchain Laws I-IV (2019-2024) | Issuances with international investor base; DLT-native CSD function |

Liechtenstein | TVTG (Token and Trusted Technologies Act, 2020) | Issuers seeking EEA passporting from a tokenization-native legal regime |

Most mid-market issuers default to eWpG in Germany or DEEP in France because the volumes do not require a DLT trading venue. Liechtenstein TVTG is common for issuers with a Swiss or international focus. The DLT Pilot becomes the right tool when an issuer plans to operate a multilateral trading facility on top of the issuance.

What does the real market actually look like?

The institutional reference points are public. The European Investment Bank issued a €100 million two-year digital bond on the Ethereum public blockchain in April 2021, placed with Goldman Sachs, Santander, and Société Générale, with cash settlement represented in a Banque de France CBDC. The EIB followed with a second €100 million digital bond in 2022 on a private blockchain. The World Bank, the Bank for International Settlements, and major commercial banks have run further pilots covering wholesale settlement, intraday repo, and tokenized money-market funds, with BlackRock's BUIDL surpassing $1 billion in tokenized money-market AUM in early 2025 and peaking near $2.9 billion by mid-year.

Below the headline issuances, the more interesting movement is in mid-market private debt. Issuers that historically could not justify the overhead of a public bond programme are using digital infrastructure to run €1 million to €50 million issuances with the same standardisation a public deal gets.

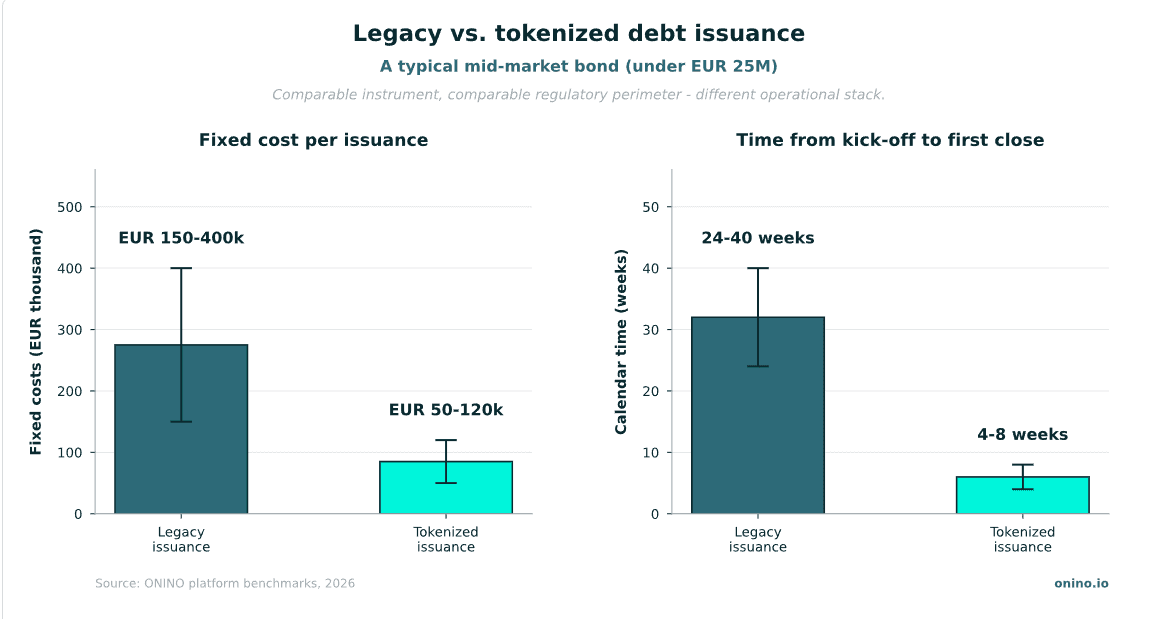

What do the economics actually look like?

A legacy bond issuance below €25 million carries roughly €150-400k in fixed costs (legal, paying agent, listing agent, registrar) and 6-10 months of calendar time. The same instrument issued on a regulated tokenized debt platform settles in roughly €50-120k of fixed costs and 4-8 weeks of calendar time once the legal structure is approved. The variable component - investor distribution - drops further because onboarded investors are reusable across offerings. This is why the mid market private debt tokenization segment is moving fastest: on a €5 million deal, the absolute cost saving is the difference between the deal being economic and not.

How long does a first tokenized bond take?

A first-time issuer typically needs 8-14 weeks from kick-off to first close: 3-4 weeks of legal structuring and prospectus work, 2-3 weeks of platform configuration and investor onboarding, then a 2-6 week offering period depending on distribution strategy. Repeat issuances on the same platform compress to 3-6 weeks total, because the legal templates and the investor base carry over.

What changes operationally when debt moves to a platform?

The same seven steps apply to any digital issuance: legal structuring, offering documentation, platform configuration, investor onboarding, offering period, register entry and instrument creation, and post-issuance servicing. The platform compresses each step.

Investor onboarding handles KYC, AML screening, and suitability checks in one flow rather than across spreadsheets and email chains. Subscription is digital and timestamped, so legal records are coherent from day one. The investor register updates in real time, removing the manual reconciliation step that produces errors at scale. Coupon payments and corporate actions execute on schedule, with audit trails attached to each event. Secondary transfers, where permitted, run through the same compliance checks the platform already enforces at primary issuance - so the post-trade workflow is not a separate system that has to be rebuilt for every offering.

"A next-generation monetary and financial system is taking shape, based on a tokenised unified ledger."

Bank for International Settlements, Annual Economic Report, press release, 24 June 2025

How is the cash leg actually settled?

Tokenizing the bond solves the securities leg. The cash leg is a separate problem and the answer determines whether settlement is genuinely atomic or just faster. Three patterns dominate in 2026.

Wholesale CBDC settlement. Used by the EIB-Banque de France issuances and ECB trial waves. Cash and securities settle on the same ledger or via coordinated DvP across central-bank infrastructure. Limited to authorised institutional participants.

Bank-issued tokenized deposits. Commercial banks issue on-chain claims against their own balance sheet. Settlement is intraday and atomic where both legs are tokenized on compatible infrastructure. Best fit for bank-to-bank flows and bank-distributed retail issuances.

Regulated euro stablecoins (MiCA e-money tokens). Used for mid-market private debt where speed matters more than wholesale-grade finality. Cash leg settles in seconds; the legal claim sits against the e-money issuer. Most common pattern outside the institutional reference deals.

The choice of cash-leg infrastructure is usually dictated by the investor base, not the issuer. A retail-distributed bond will settle differently from a wholesale placement, even on the same tokenized debt platform.

Where does liquidity actually come from?

Liquidity in private debt does not appear because an instrument is recorded digitally. Liquidity is a downstream property of the lifecycle, not a feature of the token. It appears when three conditions are met simultaneously: investors can be onboarded once and re-used across offerings, transfers can settle without re-papering the instrument, and the register is authoritative and machine-readable.

The first condition is solved by a reusable investor identity layer that travels with the investor across deals on the same platform - the second offering takes minutes to subscribe to, not days. The second condition is solved by on-chain transfer logic that carries compliance with it, so a secondary trade does not require a new compliance review for every counterparty. The third is solved by an authoritative electronic register, whether held centrally or in a DLT-based form, that the issuer, the platform, the auditor, and the regulator all read from the same source.

We refer to this internally as the ONINO Debt-Token Lifecycle: Structure, Register, Issue, Service, Transfer. Each step is fully digital, each step is auditable, and each step compresses time relative to the legacy workflow. Liquidity is a downstream property of getting all five right.

Three misconceptions about tokenized debt

"It's just crypto with extra steps." No. A tokenized bond is a regulated security under the same legal framework as a paper bond. The token is the record-keeping format, not the asset.

"Tokenization makes any debt instrument liquid." No. Liquidity requires reusable investor identity, compliant transfer logic, and an authoritative register operating together. Without those three, a tokenized bond is a faster issuance with no secondary trading - useful, but not liquid.

"You need a DLT trading venue to issue tokenized debt." No. The vast majority of European tokenized debt issuances run under national e-securities laws (eWpG, DEEP, Luxembourg blockchain laws, TVTG) without using the DLT Pilot Regime. The Pilot is only needed when secondary trading happens on a regulated DLT venue.

How does ONINO support tokenized debt issuance?

ONINO provides the regulated infrastructure for issuing and managing tokenized debt instruments across European markets. The platform handles KYC, AML and suitability checks, subscription, register management, coupon administration, corporate actions, and transfer-level compliance for senior bonds, subordinated loans, profit participation rights, and convertible notes.

Banks and asset managers operate the platform under a white-label model, offering digital debt products to their own clients under their own brand while ONINO carries the technical and compliance authorization. This pattern matters most for banks running structured-product programmes, asset managers raising private credit, and platforms that need to run multiple parallel offerings on a single compliance footprint.

Book a call

Bring your bond, subordinated loan, profit participation right, or convertible note. We will walk you through the issuance lifecycle, the regulatory path that fits your structure, and the timeline to launch.

Want to learn more how this can be applied to your business?

Read related Articles

Tokenized debt explained: how bonds, subordinated loans, and convertibles get issued under the EU DLT Pilot Regime, plus where liquidity actually comes from.